Genpact (G)

We’re cautious of Genpact. Its forecasted demand is demand over the next 12 months, suggesting a rocky road for its share price.― StockStory Analyst Team

1. News

2. Summary

Why Genpact Is Not Exciting

Originally spun off from General Electric in 2005 to provide business process services, Genpact (NYSE:G) is a global professional services firm that helps businesses transform their operations through digital technology, AI, and data analytics solutions.

- Estimated sales growth of 3.3% for the next 12 months implies demand will slow from its two-year trend

- A silver lining is that its powerful free cash flow generation enables it to reinvest its profits or return capital to investors consistently

Genpact doesn’t check our boxes. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Genpact

Genpact’s stock price of $43.59 implies a valuation ratio of 12.1x forward P/E. Yes, this valuation multiple is lower than that of other business services peers, but we’ll remind you that you often get what you pay for.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Genpact (G) Research Report: Q1 CY2025 Update

Business transformation services company Genpact (NYSE:G) met Wall Street’s revenue expectations in Q1 CY2025, with sales up 7.4% year on year to $1.21 billion. On the other hand, next quarter’s revenue guidance of $1.22 billion was less impressive, coming in 2.3% below analysts’ estimates. Its non-GAAP profit of $0.84 per share was 5.8% above analysts’ consensus estimates.

Genpact (G) Q1 CY2025 Highlights:

- Revenue: $1.21 billion vs analyst estimates of $1.21 billion (7.4% year-on-year growth, in line)

- Adjusted EPS: $0.84 vs analyst estimates of $0.79 (5.8% beat)

- Adjusted EBITDA: $220.6 million vs analyst estimates of $218.9 million (18.2% margin, 0.8% beat)

- The company dropped its revenue guidance for the full year to $4.93 billion at the midpoint from $5.08 billion, a 2.8% decrease

- Management lowered its full-year Adjusted EPS guidance to $3.47 at the midpoint, a 2.5% decrease

- Operating Margin: 15.1%, in line with the same quarter last year

- Free Cash Flow was $17.86 million, up from -$50.23 million in the same quarter last year

- Constant Currency Revenue rose 8.3% year on year (4.3% in the same quarter last year)

- Market Capitalization: $8.66 billion

Company Overview

Originally spun off from General Electric in 2005 to provide business process services, Genpact (NYSE:G) is a global professional services firm that helps businesses transform their operations through digital technology, AI, and data analytics solutions.

Genpact operates at the intersection of business process expertise and digital innovation, serving clients across financial services, consumer goods, healthcare, high tech, and manufacturing sectors. The company's services are organized into two main categories: Digital Operations Services and Data-Tech-AI Services.

In Digital Operations, Genpact embeds digital technologies, analytics, and AI into traditional business process outsourcing. This allows clients to transform functions like finance, procurement, and customer service while achieving greater flexibility and efficiency. The company's proprietary Enterprise360 intelligence platform helps clients leverage data from their operations to identify improvement opportunities.

The Data-Tech-AI Services division focuses on designing and implementing solutions that harness digital technologies, data analytics, AI, and cloud-based software. Using human-centered design principles, Genpact helps clients develop new products, create digital workspaces, and enhance engagement with customers and partners.

A manufacturing company might engage Genpact to transform its supply chain operations, using AI-powered analytics to predict demand fluctuations, optimize inventory levels, and identify potential disruptions before they occur. Similarly, a bank might work with Genpact to streamline its loan processing operations, reducing approval times while maintaining compliance with regulatory requirements.

Genpact's approach is built on its Digital Smart Enterprise Processes (Digital SEPs), a patented methodology that combines Lean Six Sigma principles with domain-specific digital technologies. The company has developed benchmarks by analyzing millions of client transactions across thousands of business processes, allowing it to identify improvement opportunities and measure effectiveness.

With delivery centers in more than 25 countries, Genpact offers clients a global delivery model with multilingual capabilities and the flexibility to work across different time zones. The company employs a "Virtual Captive" service delivery model, creating dedicated teams that function as extensions of their clients' organizations.

4. Business Process Outsourcing & Consulting

The sector stands to benefit from ongoing digital transformation, increasing corporate demand for cost efficiencies, and the growing complexity of regulatory and cybersecurity landscapes. For those that invest wisely, AI and automation capabilities could emerge as competitive advantages, enhancing process efficiencies for the companies themselves as well as their clients. On the flip side, AI could be a headwind as well as the technology could lower the barrier to entry in the space and give rise to more self-service solutions. Additional challenges in the years ahead could include wage inflation for highly skilled consultants and potential regulatory scrutiny on outsourcing practices—especially in industries like finance and healthcare where who has access to certain data matters greatly.

Genpact competes with other professional services and business process outsourcing firms including Accenture (NYSE: ACN), Cognizant (NASDAQ: CTSH), Infosys (NYSE: INFY), and Tata Consultancy Services (NSE: TCS), as well as with the consulting arms of major accounting firms like Deloitte and EY.

5. Sales Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $4.85 billion in revenue over the past 12 months, Genpact is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Genpact’s 5.9% annualized revenue growth over the last five years was decent. This shows its offerings generated slightly more demand than the average business services company, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Genpact’s annualized revenue growth of 5.1% over the last two years aligns with its five-year trend, suggesting its demand was stable.

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 5.4% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that Genpact has properly hedged its foreign currency exposure.

This quarter, Genpact grew its revenue by 7.4% year on year, and its $1.21 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 3.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.6% over the next 12 months, similar to its two-year rate. This projection is above the sector average and implies its newer products and services will catalyze better top-line performance.

6. Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Genpact has been an efficient company over the last five years. It was one of the more profitable businesses in the business services sector, boasting an average adjusted operating margin of 16.7%.

Analyzing the trend in its profitability, Genpact’s adjusted operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Genpact generated an adjusted operating profit margin of 17.3%, up 1.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Genpact’s EPS grew at a solid 9.5% compounded annual growth rate over the last five years, higher than its 5.9% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its adjusted operating margin didn’t expand.

Diving into the nuances of Genpact’s earnings can give us a better understanding of its performance. A five-year view shows that Genpact has repurchased its stock, shrinking its share count by 9.2%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, Genpact reported EPS at $0.84, up from $0.73 in the same quarter last year. This print beat analysts’ estimates by 5.8%. Over the next 12 months, Wall Street expects Genpact’s full-year EPS of $3.39 to grow 6.2%.

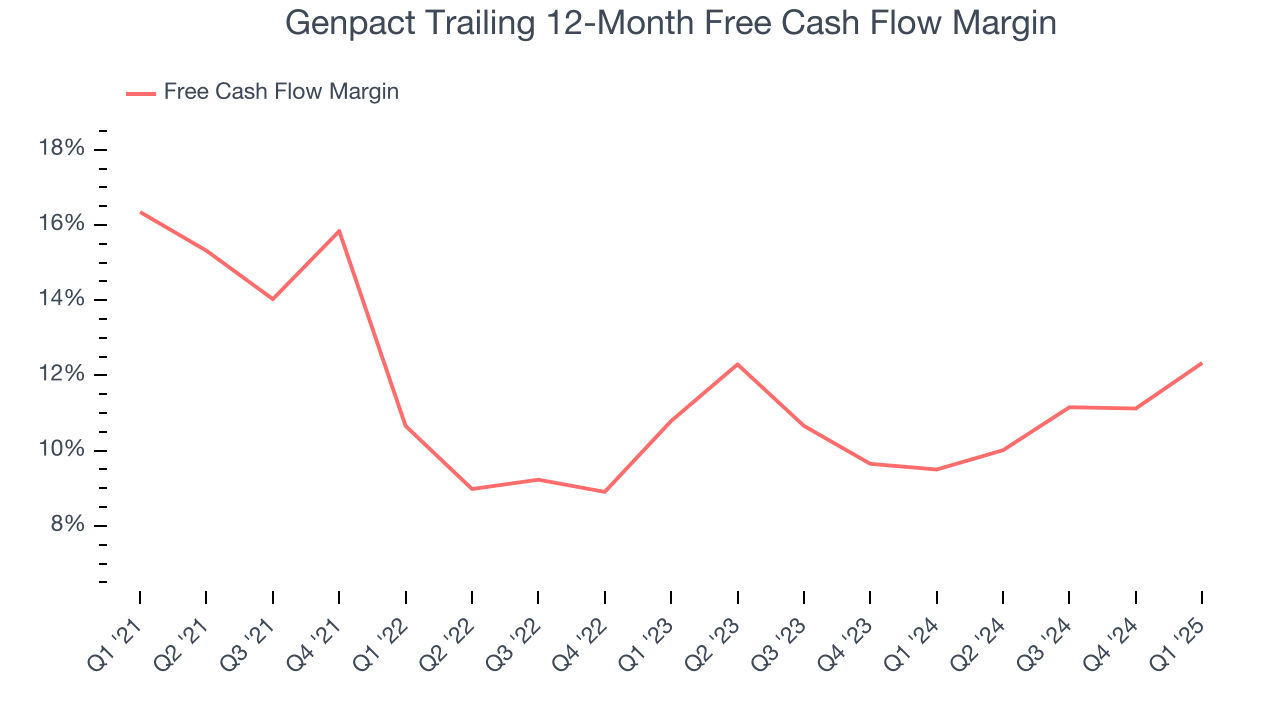

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Genpact has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 11.8% over the last five years, quite impressive for a business services business.

Taking a step back, we can see that Genpact’s margin dropped by 4 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity.

Genpact’s free cash flow clocked in at $17.86 million in Q1, equivalent to a 1.5% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Genpact hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked. Its five-year average ROIC was 17.6%, higher than most business services businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Genpact’s ROIC has increased. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

10. Balance Sheet Assessment

Genpact reported $561.6 million of cash and $1.42 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $924.7 million of EBITDA over the last 12 months, we view Genpact’s 0.9× net-debt-to-EBITDA ratio as safe. We also see its $48.42 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Genpact’s Q1 Results

It was encouraging to see Genpact beat analysts’ constant currency revenue and EPS expectations this quarter. On the other hand, it lowered its full-year revenue and EPS guidance. Overall, this was a softer quarter. The stock traded down 15.3% to $41.99 immediately following the results.

12. Is Now The Time To Buy Genpact?

Updated: June 13, 2025 at 12:08 AM EDT

When considering an investment in Genpact, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Genpact isn’t a terrible business, but it doesn’t pass our bar. Although its revenue growth was decent over the last five years, it’s expected to deteriorate over the next 12 months and its cash profitability fell over the last five years.

Genpact’s P/E ratio based on the next 12 months is 12.1x. This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $50.98 on the company (compared to the current share price of $43.59).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.