Bristol-Myers Squibb (BMY)

We’re skeptical of Bristol-Myers Squibb. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why Bristol-Myers Squibb Is Not Exciting

With roots dating back to 1887 and a transformative merger in 1989 that gave the company its current name, Bristol-Myers Squibb (NYSE:BMY) discovers, develops, and markets prescription medications for serious diseases including cancer, blood disorders, immunological conditions, and cardiovascular diseases.

- Estimated sales decline of 4.4% for the next 12 months implies a challenging demand environment

- Below-average returns on capital indicate management struggled to find compelling investment opportunities, and its shrinking returns suggest its past profit sources are losing steam

- On the bright side, its sizeable revenue base of $47.64 billion gives it economies of scale and advantages over new entrants due to the industry’s regulatory complexity

Bristol-Myers Squibb’s quality is lacking. We believe there are better businesses elsewhere.

Why There Are Better Opportunities Than Bristol-Myers Squibb

Bristol-Myers Squibb is trading at $48.46 per share, or 7.3x forward P/E. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Bristol-Myers Squibb (BMY) Research Report: Q1 CY2025 Update

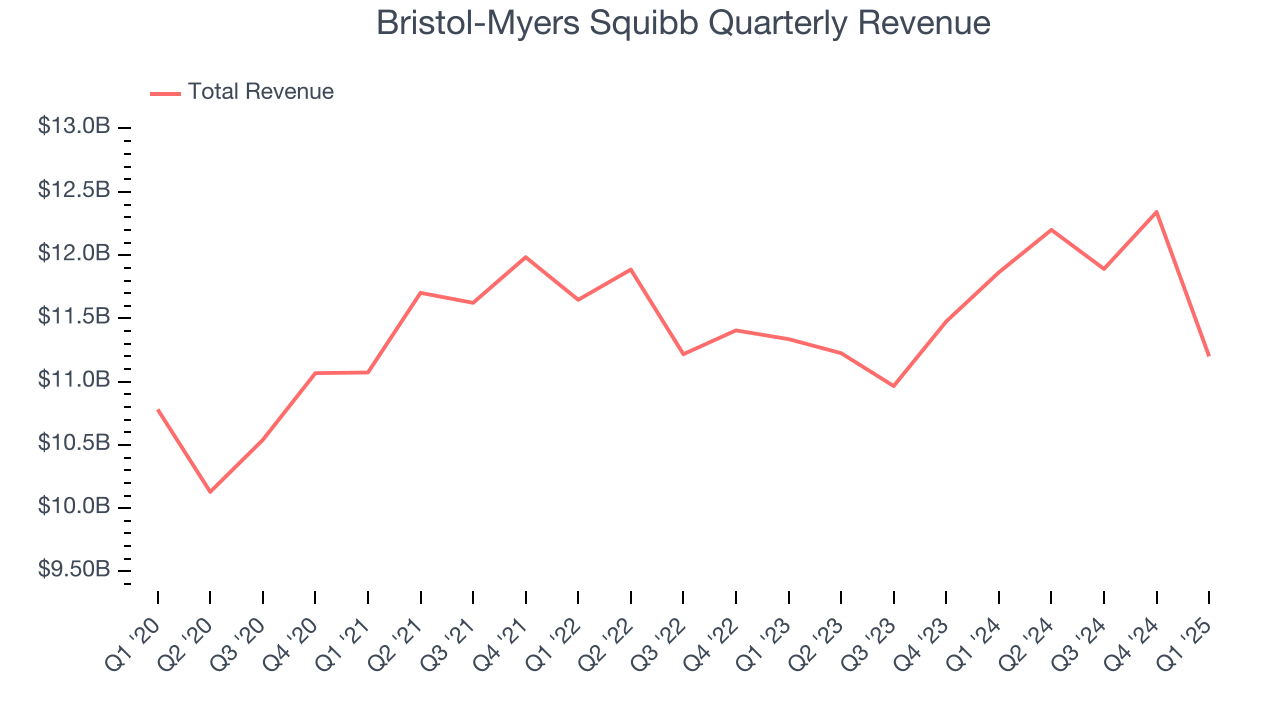

Biopharmaceutical company Bristol Myers Squibb (NYSE:BMY) announced better-than-expected revenue in Q1 CY2025, but sales fell by 5.6% year on year to $11.2 billion. The company’s full-year revenue guidance of $46.3 billion at the midpoint came in 1.2% above analysts’ estimates. Its non-GAAP profit of $1.80 per share was 19.9% above analysts’ consensus estimates.

Bristol-Myers Squibb (BMY) Q1 CY2025 Highlights:

- Revenue: $11.2 billion vs analyst estimates of $10.78 billion (5.6% year-on-year decline, 3.9% beat)

- Adjusted EPS: $1.80 vs analyst estimates of $1.50 (19.9% beat)

- The company lifted its revenue guidance for the full year to $46.3 billion at the midpoint from $45.5 billion, a 1.8% increase

- Management raised its full-year Adjusted EPS guidance to $6.85 at the midpoint, a 2.2% increase

- Market Capitalization: $98.75 billion

Company Overview

With roots dating back to 1887 and a transformative merger in 1989 that gave the company its current name, Bristol-Myers Squibb (NYSE:BMY) discovers, develops, and markets prescription medications for serious diseases including cancer, blood disorders, immunological conditions, and cardiovascular diseases.

Bristol-Myers Squibb operates at the intersection of pharmaceutical scale and biotech innovation, focusing on creating transformational medicines for patients with serious diseases. The company's portfolio spans several therapeutic areas, with particularly strong positions in oncology, hematology, immunology, cardiovascular, and neuroscience.

Among its key products is Eliquis, an oral anticoagulant used to reduce stroke risk in patients with atrial fibrillation and treat blood clots. In oncology, Opdivo is a cornerstone immunotherapy that works by helping the immune system detect and fight cancer cells across multiple tumor types. For autoimmune conditions, Orencia treats rheumatoid arthritis and psoriatic arthritis by modulating immune system activity.

The company's business model involves extensive research and development, with annual R&D investments of billions of dollars to fuel its pipeline of potential new treatments. When a physician prescribes a Bristol-Myers Squibb medication for a patient with advanced melanoma, for instance, the drug is typically distributed through specialty pharmacies or wholesalers before reaching the patient.

Bristol-Myers Squibb generates revenue primarily through prescription drug sales to wholesalers, specialty distributors, and pharmacies. The company employs a global sales force that educates healthcare professionals about its products, while also working to secure placement on insurance formularies and reimbursement plans.

The company has expanded its portfolio through strategic acquisitions, including Celgene in 2019, which brought the multiple myeloma treatment Revlimid into its lineup, and more recently Turning Point Therapeutics, which added precision oncology capabilities. Bristol-Myers Squibb maintains significant manufacturing operations across the United States, Puerto Rico, and several European countries, with products sold worldwide.

4. Branded Pharmaceuticals

The branded pharmaceutical industry relies on a high-cost, high-reward business model, driven by substantial investments in research and development to create innovative, patent-protected drugs. Successful products can generate significant revenue streams over their patent life, and the larger a roster of drugs, the stronger a moat a company enjoys. However, the business model is inherently risky, with high failure rates during clinical trials, lengthy regulatory approval processes, and intense competition from generic and biosimilar manufacturers once patents expire. These challenges, combined with scrutiny over drug pricing, create a complex operating environment. Looking ahead, the industry is positioned for tailwinds from advancements in precision medicine, increasing adoption of AI to enhance drug development efficiency, and growing global demand for treatments addressing chronic and rare diseases. However, headwinds include heightened regulatory scrutiny, pricing pressures from governments and insurers, and the looming patent cliffs for key blockbuster drugs. Patent cliffs bring about competition from generics, forcing branded pharmaceutical companies back to the drawing board to find the next big thing.

Bristol-Myers Squibb competes with other major pharmaceutical companies including Merck (NYSE:MRK), Pfizer (NYSE:PFE), Novartis (NYSE:NVS), AstraZeneca (NASDAQ:AZN), and Roche (OTCQX:RHHBY), particularly in oncology and immunology therapeutic areas.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $47.64 billion in revenue over the past 12 months, Bristol-Myers Squibb boasts impressive economies of scale. It may not be as large as heavyweights such as UnitedHealth Group and The Cigna Group from a topline perspective, but its heft is still an important advantage in a healthcare industry that is heavily regulated, complex, and resource-intensive.

6. Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Bristol-Myers Squibb’s 9% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Bristol-Myers Squibb’s recent performance shows its demand has slowed as its annualized revenue growth of 1.9% over the last two years was below its five-year trend.

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Growth Portfolio. Over the last two years, Bristol-Myers Squibb’s Growth Portfolio revenue averaged 17.5% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, Bristol-Myers Squibb’s revenue fell by 5.6% year on year to $11.2 billion but beat Wall Street’s estimates by 3.9%.

Looking ahead, sell-side analysts expect revenue to decline by 5.4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Bristol-Myers Squibb was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.7% was weak for a healthcare business.

On the plus side, Bristol-Myers Squibb’s operating margin rose by 6.4 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 6.4 percentage points on a two-year basis. If Bristol-Myers Squibb wants to pass our bar, it must prove it can expand its profitability consistently.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Bristol-Myers Squibb’s EPS grew at a decent 6.7% compounded annual growth rate over the last five years. Despite its operating margin expansion and share repurchases during that time, this performance was lower than its 9% annualized revenue growth, telling us the delta came from reduced interest expenses or taxes.

In Q1, Bristol-Myers Squibb reported EPS at $1.80, up from negative $4.40 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Bristol-Myers Squibb’s full-year EPS of $7.34 to shrink by 9.6%.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Bristol-Myers Squibb has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the healthcare sector, averaging 29.1% over the last five years. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Bristol-Myers Squibb’s margin expanded by 1 percentage points during that time. This is encouraging because it gives the company more optionality.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Bristol-Myers Squibb historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.4%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Bristol-Myers Squibb’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

Bristol-Myers Squibb reported $11.78 billion of cash and $49.71 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $25.79 billion of EBITDA over the last 12 months, we view Bristol-Myers Squibb’s 1.5× net-debt-to-EBITDA ratio as safe. We also see its $1.24 billion of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Bristol-Myers Squibb’s Q1 Results

We enjoyed seeing Bristol-Myers Squibb beat analysts’ revenue and EPS expectations this quarter. We were also glad it lifted its full-year guidance for both metrics. Zooming out, we think this was a solid "beat-and-raise" quarter. The stock traded up 1.3% to $49.12 immediately following the results.

13. Is Now The Time To Buy Bristol-Myers Squibb?

Updated: June 7, 2025 at 11:33 PM EDT

Before deciding whether to buy Bristol-Myers Squibb or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Bristol-Myers Squibb isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was decent over the last five years, it’s expected to deteriorate over the next 12 months and its diminishing returns show management's prior bets haven't worked out. And while the company’s scale makes it a trusted partner with negotiating leverage, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Bristol-Myers Squibb’s P/E ratio based on the next 12 months is 7.3x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $57.10 on the company (compared to the current share price of $48.46).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.