Comfort Systems (FIX)

Not many stocks excite us like Comfort Systems. Its exceptional revenue growth and returns on capital show it can expand quickly and profitably.― StockStory Analyst Team

1. News

2. Summary

Why We Like Comfort Systems

Formed through the merger of 12 companies, Comfort Systems (NYSE:FIX) provides mechanical and electrical contracting services.

- Annual revenue growth of 21.4% over the last five years was superb and indicates its market share increased during this cycle

- Earnings per share have massively outperformed its peers over the last five years, increasing by 40.5% annually

- Market-beating returns on capital illustrate that management has a knack for investing in profitable ventures, and its returns are growing as it capitalizes on even better market opportunities

Comfort Systems is a remarkable business. The price seems reasonable based on its quality, and we think now is an opportune time to buy the stock.

Why Is Now The Time To Buy Comfort Systems?

Comfort Systems’s stock price of $498.63 implies a valuation ratio of 26.7x forward P/E. Valuation is above that of many industrials companies, but we think the price is justified given its business fundamentals.

Entry price may seem important in the moment, but our work shows that time and again, long-term market outperformance is determined by business quality rather than getting an absolute bargain on a stock.

3. Comfort Systems (FIX) Research Report: Q1 CY2025 Update

HVAC and electrical contractor Comfort Systems (NYSE:FIX) reported Q1 CY2025 results beating Wall Street’s revenue expectations, with sales up 19.1% year on year to $1.83 billion. Its GAAP profit of $4.75 per share was 28.1% above analysts’ consensus estimates.

Comfort Systems (FIX) Q1 CY2025 Highlights:

- Revenue: $1.83 billion vs analyst estimates of $1.76 billion (19.1% year-on-year growth, 4.2% beat)

- EPS (GAAP): $4.75 vs analyst estimates of $3.71 (28.1% beat)

- Adjusted EBITDA: $242.7 million vs analyst estimates of $200.7 million (13.3% margin, 20.9% beat)

- Operating Margin: 11.4%, up from 8.8% in the same quarter last year

- Free Cash Flow was -$109.1 million, down from $122.6 million in the same quarter last year

- Backlog: $6.89 billion at quarter end, up 16.5% year on year

- Market Capitalization: $12.54 billion

Company Overview

Formed through the merger of 12 companies, Comfort Systems (NYSE:FIX) provides mechanical and electrical contracting services.

The company specializes in the design, installation, maintenance, and repair of heating, ventilation, air conditioning (HVAC), and electrical systems for commercial, industrial, and institutional buildings across the United States. How else would the typical American office building keep its workers chilly and in need of a sweater during the sweltering summer months?

Additional product offerings include building automation and controls, energy retrofitting, plumbing and piping solutions, indoor air quality improvement equipment, and electrical and lighting services. Many of these are top-of-mind for customers who want to digitize their operations or improve energy efficiency efforts.

Historically, a major percentage of the company’s total revenue is attributed to installation services within newly-constructed facilities. Another meaningful portion of revenue is from the renovation, expansion, maintenance, repair, and replacement of its equipment in existing buildings. In addition to organic growth, acquisitions have also contributed to Comfort Systems' growth. For example, the company acquired electrical contracting service company Amteck in 2021 as well as a number of acquisitions in 2024.

4. Construction and Maintenance Services

Construction and maintenance services companies not only boast technical know-how in specialized areas but also may hold special licenses and permits. Those who work in more regulated areas can enjoy more predictable revenue streams - for example, fire escapes need to be inspected every five years. More recently, services to address energy efficiency and labor availability are also creating incremental demand. But like the broader industrials sector, construction and maintenance services companies are at the whim of economic cycles as external factors like interest rates can greatly impact the new construction that drives incremental demand for these companies’ offerings.

Comfort Systems USA's top competitors include EMCOR (NYSE:EME), Johnson Controls (NYSE:JCI), and Trane Technologies (NYSE:TT).

5. Sales Growth

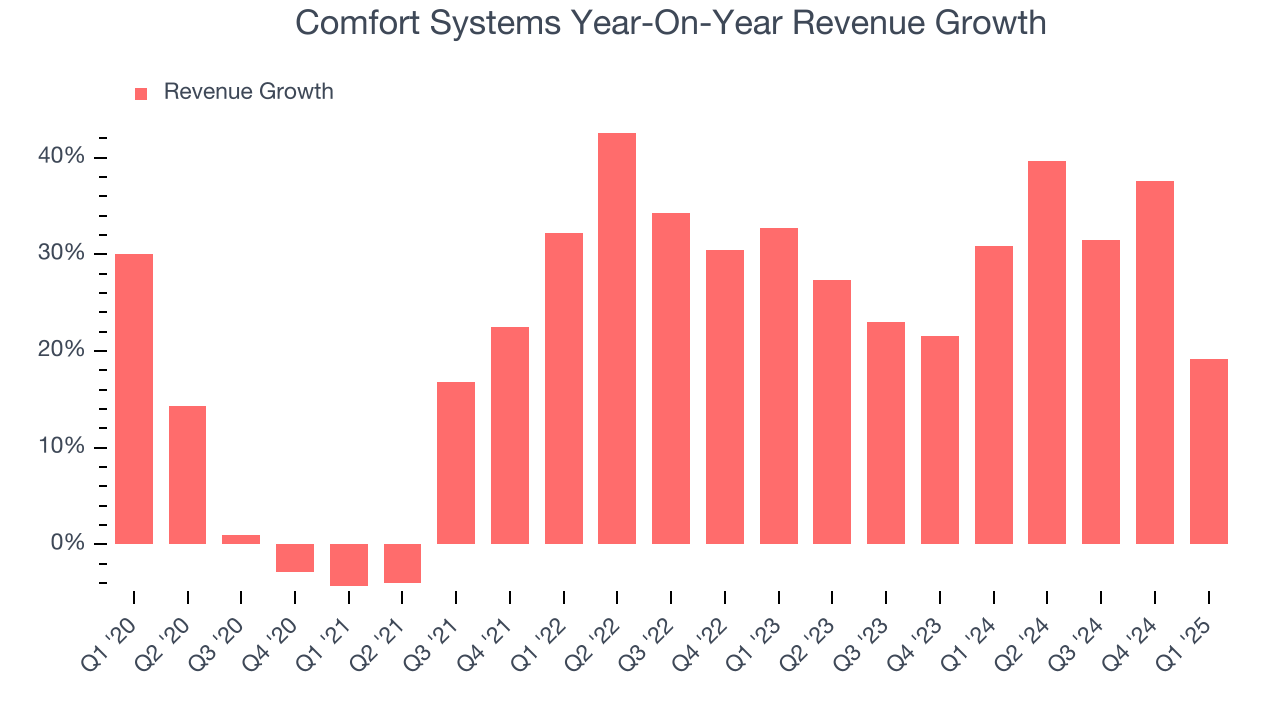

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Comfort Systems’s sales grew at an incredible 21.4% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Comfort Systems’s annualized revenue growth of 28.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated. We note Comfort Systems isn’t alone in its success as the Construction and Maintenance Services industry experienced a boom, with many similar businesses also posting double-digit growth.

Comfort Systems also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Comfort Systems’s backlog reached $6.89 billion in the latest quarter and averaged 30.5% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Comfort Systems’s products and services but raises concerns about capacity constraints.

This quarter, Comfort Systems reported year-on-year revenue growth of 19.1%, and its $1.83 billion of revenue exceeded Wall Street’s estimates by 4.2%.

Looking ahead, sell-side analysts expect revenue to grow 6.5% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

6. Gross Margin & Pricing Power

Comfort Systems has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 19.6% gross margin over the last five years. Said differently, Comfort Systems had to pay a chunky $80.38 to its suppliers for every $100 in revenue.

Comfort Systems produced a 22% gross profit margin in Q1, marking a 2.7 percentage point increase from 19.3% in the same quarter last year. Comfort Systems’s full-year margin has also been trending up over the past 12 months, increasing by 2.2 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Comfort Systems has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.5%, higher than the broader industrials sector.

Looking at the trend in its profitability, Comfort Systems’s operating margin rose by 4.1 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Comfort Systems generated an operating profit margin of 11.4%, up 2.6 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Comfort Systems’s EPS grew at an astounding 40.6% compounded annual growth rate over the last five years, higher than its 21.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Comfort Systems’s earnings can give us a better understanding of its performance. As we mentioned earlier, Comfort Systems’s operating margin expanded by 4.1 percentage points over the last five years. On top of that, its share count shrank by 3.5%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Comfort Systems, its two-year annual EPS growth of 66.4% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Comfort Systems reported EPS at $4.75, up from $2.69 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Comfort Systems’s full-year EPS of $16.67 to grow 11%.

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Comfort Systems has shown impressive cash profitability, enabling it to ride out cyclical downturns more easily while maintaining its investments in new and existing offerings. The company’s free cash flow margin averaged 7.9% over the last five years, better than the broader industrials sector.

Taking a step back, we can see that Comfort Systems’s margin dropped by 4.7 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Comfort Systems burned through $109.1 million of cash in Q1, equivalent to a negative 6% margin. The company’s cash flow turned negative after being positive in the same quarter last year, which isn’t ideal considering its longer-term trend.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Comfort Systems’s five-year average ROIC was 26.3%, placing it among the best industrials companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Comfort Systems’s ROIC has increased significantly over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Comfort Systems is a profitable, well-capitalized company with $204.8 million of cash and $67.84 million of debt on its balance sheet. This $136.9 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Comfort Systems’s Q1 Results

We were impressed by how significantly Comfort Systems blew past analysts’ backlog expectations this quarter. We were also excited its EPS outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid quarter. The stock traded up 10.2% to $415 immediately following the results.

13. Is Now The Time To Buy Comfort Systems?

Updated: June 5, 2025 at 11:02 PM EDT

Before making an investment decision, investors should account for Comfort Systems’s business fundamentals and valuation in addition to what happened in the latest quarter.

Comfort Systems is one of the best industrials companies out there. For starters, its revenue growth was exceptional over the last five years. And while its cash profitability fell over the last five years, its backlog growth has been marvelous. On top of that, Comfort Systems’s astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

Comfort Systems’s P/E ratio based on the next 12 months is 26.8x. Analyzing the industrials landscape today, Comfort Systems’s positive attributes shine bright. We think it’s one of the best businesses in our coverage and like the stock at this price.

Wall Street analysts have a consensus one-year price target of $514.17 on the company (compared to the current share price of $499.16), implying they see 3% upside in buying Comfort Systems in the short term.