Apogee (APOG)

We’re cautious of Apogee. Its weak gross margin and failure to generate revenue growth show it lacks demand and decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why We Think Apogee Will Underperform

Involved in the design of the Apple Store on Fifth Avenue in New York City, Apogee (NASDAQ:APOG) sells architectural products and services such as high-performance glass for commercial buildings.

- Sales stagnated over the last five years and signal the need for new growth strategies

- Estimated sales for the next 12 months are flat and imply a softer demand environment

- A consolation is that its earnings growth has beaten its peers over the last five years as its EPS has compounded at 15.8% annually

Apogee doesn’t check our boxes. We believe there are better businesses elsewhere.

Why There Are Better Opportunities Than Apogee

At $38.66 per share, Apogee trades at 9.1x forward P/E. Apogee’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Apogee (APOG) Research Report: Q1 CY2025 Update

Architectural products company Apogee (NASDAQ:APOG) reported Q1 CY2025 results exceeding the market’s revenue expectations, but sales fell by 4.5% year on year to $345.7 million. The company’s full-year revenue guidance of $1.4 billion at the midpoint came in 2% above analysts’ estimates. Its non-GAAP profit of $0.89 per share was 2.3% above analysts’ consensus estimates.

Apogee (APOG) Q1 CY2025 Highlights:

- Revenue: $345.7 million vs analyst estimates of $331.8 million (4.5% year-on-year decline, 4.2% beat)

- Adjusted EPS: $0.89 vs analyst estimates of $0.87 (2.3% beat)

- Adjusted EBITDA: $41.11 million vs analyst estimates of $37.46 million (11.9% margin, 9.7% beat)

- Management’s revenue guidance for the upcoming financial year 2026 is $1.4 billion at the midpoint, beating analyst estimates by 2% and implying 2.9% growth (vs -3.9% in FY2025)

- Adjusted EPS guidance for the upcoming financial year 2026 is $3.83 at the midpoint, missing analyst estimates by 10.5%

- Operating Margin: 1.8%, down from 9.5% in the same quarter last year

- Free Cash Flow Margin: 5.5%, down from 16.2% in the same quarter last year

- Market Capitalization: $1.01 billion

Company Overview

Involved in the design of the Apple Store on Fifth Avenue in New York City, Apogee (NASDAQ:APOG) sells architectural products and services such as high-performance glass for commercial buildings.

The company designs and manufactures the materials used in architectural designs that range from the mundane to the world-famous. Its building projects are usually found in commercial or industrial buildings rather than residential ones, and its key customers include builders and contractors.

Apogee’s offerings can be classified into several categories. Architectural products include architectural glass, aluminum windows, curtain walls, storefronts, and entrance systems. Architectural services include designs and installation of the aforementioned products. Lastly, the company offers custom framing and technical display applications like the glass used in Apple Stores or the frames used in renowned museums worldwide.

The company generates revenue through selling physical products; services are a much smaller portion of total revenue. As mentioned, Apogee sells its products and services to builders, contractors, architects, and developers involved in the construction of offices, stores, and institutional buildings.

4. Commercial Building Products

Commercial building products companies, which often serve more complicated projects, can supplement their core business with higher-margin installation and consulting services revenues. More recently, advances to address labor availability and job site productivity have spurred innovation. Additionally, companies in the space that can produce more energy-efficient materials have opportunities to take share. However, these companies are at the whim of commercial construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of commercial building products companies.

Other companies in the architectural glass and building products industry include Tecnoglass (NYSE:TGLS) and private companies Oldcastle BuildingEvelope, Vitro Architectural Glass, and Guardian Glass.

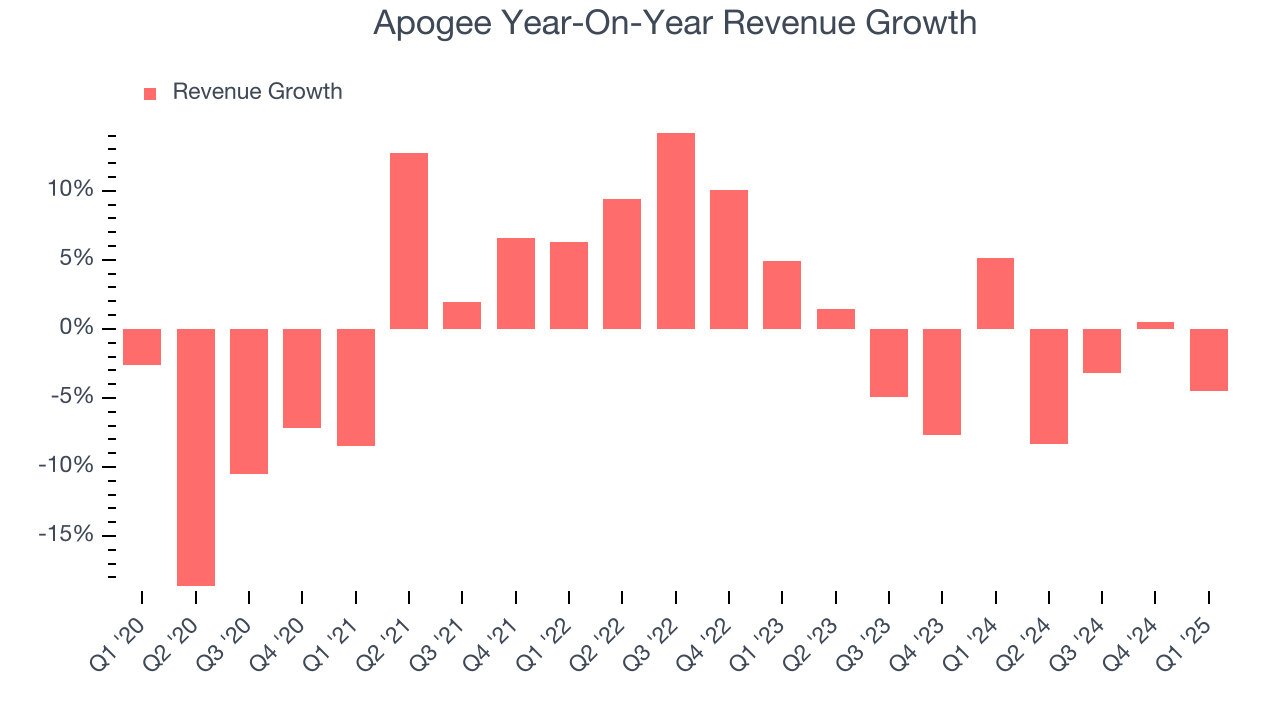

5. Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Apogee struggled to consistently increase demand as its $1.36 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and suggests it’s a lower quality business.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Apogee’s recent performance shows its demand remained suppressed as its revenue has declined by 2.8% annually over the last two years. Apogee isn’t alone in its struggles as the Commercial Building Products industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, Apogee’s revenue fell by 4.5% year on year to $345.7 million but beat Wall Street’s estimates by 4.2%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

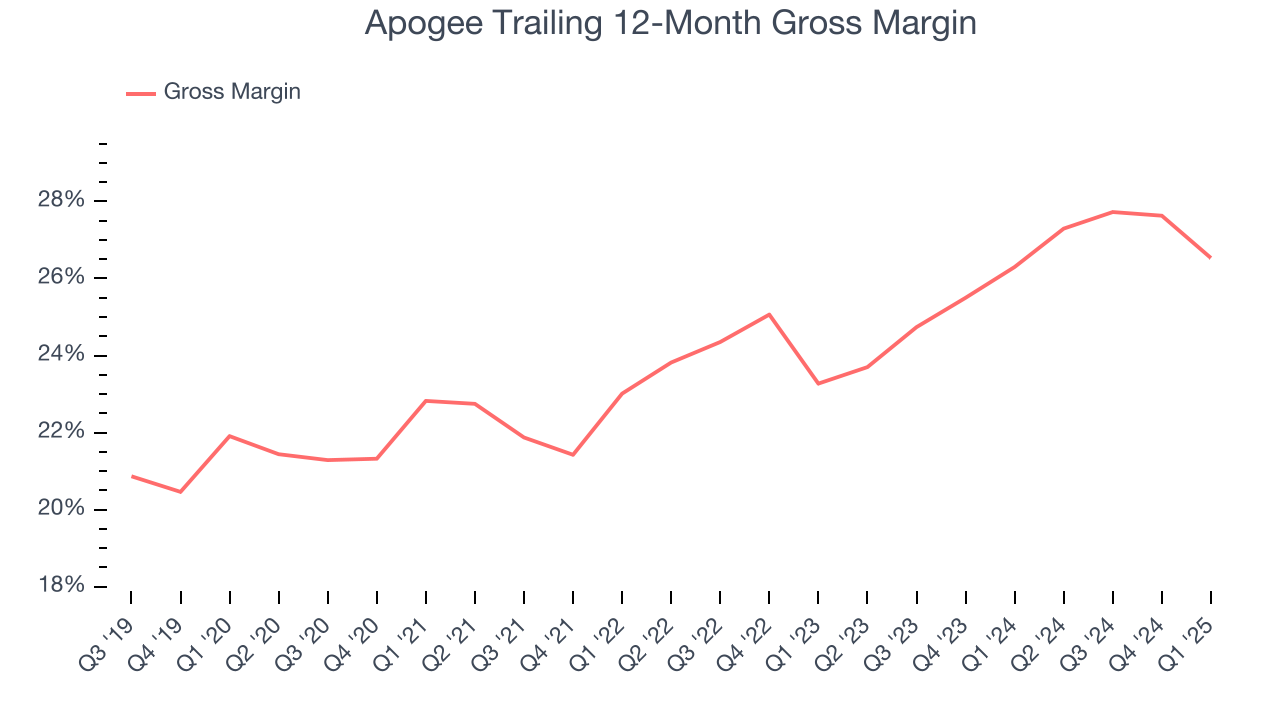

6. Gross Margin & Pricing Power

Apogee has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 24.4% gross margin over the last five years. That means Apogee paid its suppliers a lot of money ($75.57 for every $100 in revenue) to run its business.

In Q1, Apogee produced a 21.6% gross profit margin, marking a 4.4 percentage point decrease from 26% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

Apogee has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.4%, higher than the broader industrials sector.

Analyzing the trend in its profitability, Apogee’s operating margin rose by 3.1 percentage points over the last five years, showing its efficiency has improved.

In Q1, Apogee generated an operating profit margin of 1.8%, down 7.7 percentage points year on year. Since Apogee’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

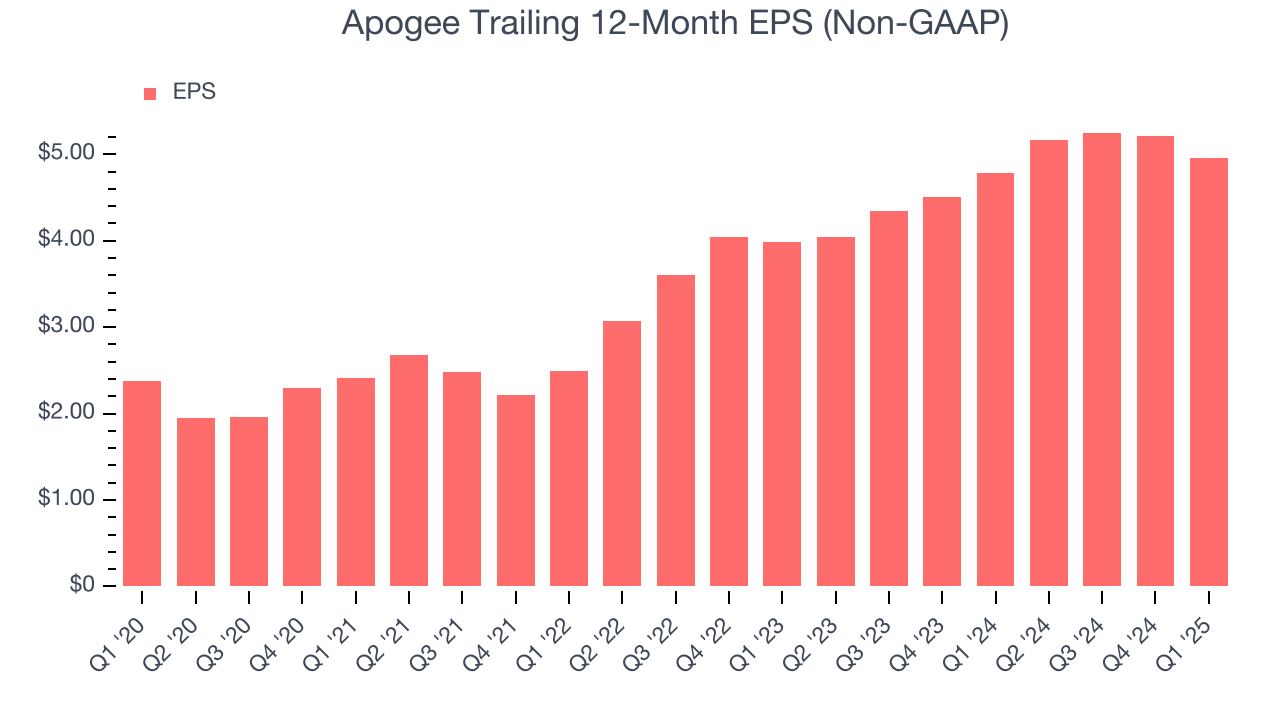

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Apogee’s EPS grew at a spectacular 15.8% compounded annual growth rate over the last five years, higher than its flat revenue. This tells us management responded to softer demand by adapting its cost structure.

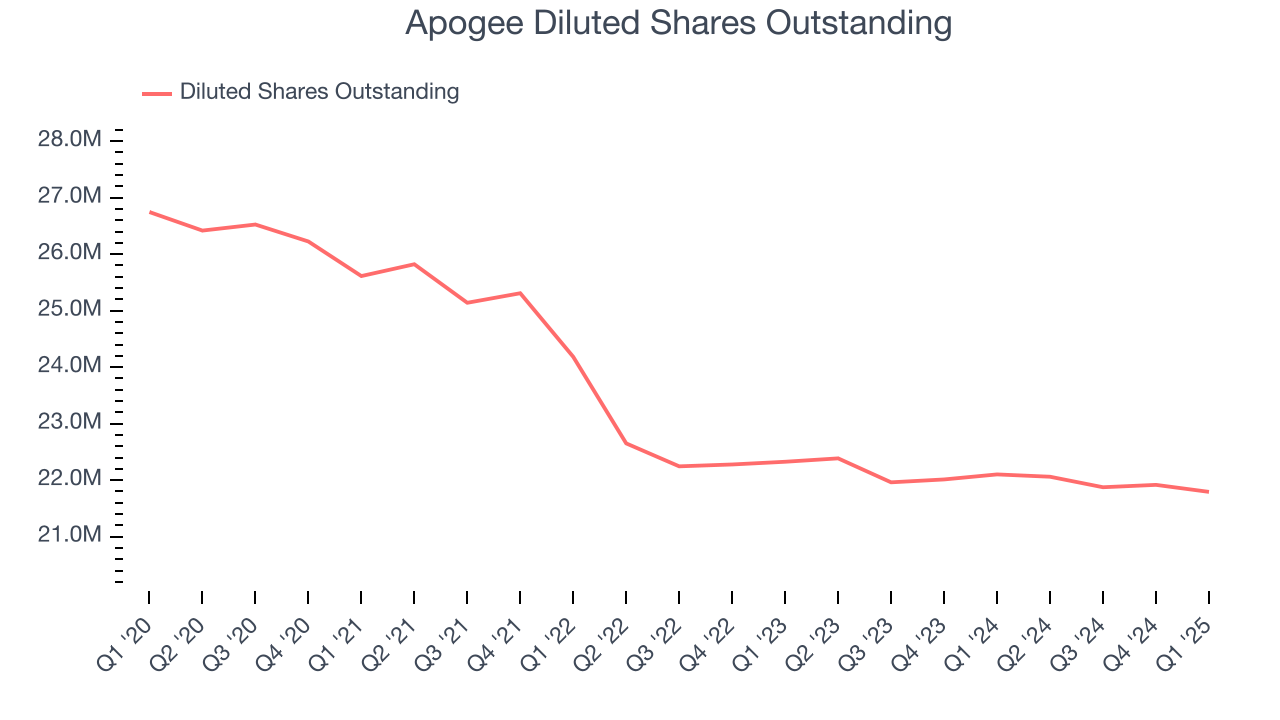

Diving into Apogee’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Apogee’s operating margin declined this quarter but expanded by 3.1 percentage points over the last five years. Its share count also shrank by 18.5%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Apogee, its two-year annual EPS growth of 11.5% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q1, Apogee reported EPS at $0.89, down from $1.14 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 2.3%. Over the next 12 months, Wall Street expects Apogee’s full-year EPS of $4.96 to shrink by 14.5%.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Apogee has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.4% over the last five years, slightly better than the broader industrials sector.

Taking a step back, we can see that Apogee’s margin dropped by 2.8 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Apogee’s free cash flow clocked in at $19.14 million in Q1, equivalent to a 5.5% margin. The company’s cash profitability regressed as it was 10.7 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Apogee hasn’t been the highest-quality company lately because of its poor top-line performance, it historically found a few growth initiatives that worked out well. Its five-year average ROIC was 15.8%, impressive for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Apogee’s ROIC averaged 3.4 percentage point increases each year. This is a good sign, and we hope the company can keep improving.

11. Balance Sheet Assessment

Apogee reported $41.45 million of cash and $851.9 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $192.7 million of EBITDA over the last 12 months, we view Apogee’s 4.2× net-debt-to-EBITDA ratio as safe. We also see its $891,000 of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Apogee’s Q1 Results

We were impressed by how significantly Apogee blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EPS guidance missed significantly. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $45.90 immediately after reporting.

13. Is Now The Time To Buy Apogee?

Updated: May 24, 2025 at 10:59 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Apogee.

Apogee isn’t a terrible business, but it doesn’t pass our bar. To kick things off, its revenue growth was weak over the last five years, and analysts don’t see anything changing over the next 12 months. And while its spectacular EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its projected EPS for the next year is lacking. On top of that, its cash profitability fell over the last five years.

Apogee’s P/E ratio based on the next 12 months is 9.1x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $55 on the company (compared to the current share price of $38.66).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.

Want to invest in a High Quality big tech company? We’d point you in the direction of Microsoft and Google, which have durable competitive moats and strong fundamentals, factors that are large determinants of long-term market outperformance.

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist. We typically have quarterly earnings results analyzed within seconds of the data being released, giving investors the chance to react before the market has fully absorbed the information. This is especially true for companies reporting pre-market.