Brookdale (BKD)

Brookdale is in for a bumpy ride. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Brookdale Will Underperform

With a network of over 650 communities serving approximately 59,000 residents across 41 states, Brookdale Senior Living (NYSE:BKD) operates senior living communities across the United States, offering independent living, assisted living, memory care, and continuing care retirement communities.

- Customers postponed purchases of its products and services this cycle as its revenue declined by 4.8% annually over the last five years

- ROIC of -0.8% reflects management’s challenges in identifying attractive investment opportunities

- Depletion of cash reserves could lead to a fundraising event that triggers shareholder dilution

Brookdale falls below our quality standards. Better businesses are for sale in the market.

Why There Are Better Opportunities Than Brookdale

Brookdale’s stock price of $6.90 implies a valuation ratio of 3.6x forward EV-to-EBITDA. Brookdale’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Brookdale (BKD) Research Report: Q1 CY2025 Update

Senior living provider Brookdale Senior Living (NYSE:BKD) met Wall Street’s revenue expectations in Q1 CY2025, with sales up 4% year on year to $813.9 million. Its GAAP loss of $0.28 per share was significantly below analysts’ consensus estimates.

Brookdale (BKD) Q1 CY2025 Highlights:

- Revenue: $813.9 million vs analyst estimates of $816.9 million (4% year-on-year growth, in line)

- EPS (GAAP): -$0.28 vs analyst estimates of -$0.11 (significant miss)

- Adjusted EBITDA: $124.1 million vs analyst estimates of $112.8 million (15.3% margin, 10% beat)

- EBITDA guidance for the full year is $445 million at the midpoint, above analyst estimates of $440.4 million

- Operating Margin: 3.6%, in line with the same quarter last year

- Free Cash Flow was -$18.42 million compared to -$45.55 million in the same quarter last year

- Market Capitalization: $1.33 billion

Company Overview

With a network of over 650 communities serving approximately 59,000 residents across 41 states, Brookdale Senior Living (NYSE:BKD) operates senior living communities across the United States, offering independent living, assisted living, memory care, and continuing care retirement communities.

Brookdale's communities are designed to provide seniors with a continuum of care that allows them to "age in place" as their needs change over time. The company's facilities range from large multi-story buildings with extensive amenities for more independent seniors to specialized memory care neighborhoods designed specifically for residents with dementia and Alzheimer's disease.

Independent living residents at Brookdale receive basic services like dining options, emergency alert systems, housekeeping, and recreational activities while maintaining their autonomy. As residents require more assistance, they can transition to assisted living, where 24-hour staff help with activities of daily living (ADLs) such as bathing, dressing, and medication management. For those with cognitive impairments, Brookdale's memory care units provide specialized environments with higher levels of supervision and tailored activities.

Continuing Care Retirement Communities (CCRCs) represent Brookdale's most comprehensive offering, with multiple levels of care available on a single campus. A resident might initially move into independent living and later transfer to assisted living or skilled nursing as health needs evolve, all without leaving the community.

Brookdale generates revenue primarily through monthly service fees paid by residents, with rates varying based on the level of care provided. The company also manages properties on behalf of third-party owners, collecting management fees typically calculated as a percentage of the community's gross revenue.

The senior living industry experiences some seasonality, with occupancy often declining in winter months due to illness and weather concerns before rebounding in spring and summer. Brookdale's operations are subject to extensive regulation, including healthcare laws governing financial arrangements and privacy requirements for handling resident health information.

4. Senior Health, Home Health & Hospice

The senior health, home care, and hospice care industries provide essential services to aging populations and patients with chronic or terminal conditions. These companies benefit from stable, recurring revenue driven by relationships with patients and families that can extend many months or even years. However, the labor-intensive nature of the business makes it vulnerable to rising labor costs and staffing shortages, while profitability is constrained by reimbursement rates from Medicare, Medicaid, and private insurers. Looking ahead, the industry is positioned for tailwinds from an aging population, increasing chronic disease prevalence, and a growing preference for personalized in-home care. Advancements in remote monitoring and telehealth are expected to enhance efficiency and care delivery. However, headwinds such as labor shortages, wage inflation, and regulatory uncertainty around reimbursement could pose challenges. Investments in digitization and technology-driven care will be critical for long-term success.

Brookdale's main competitors in the senior living industry include Atria Senior Living, Life Care Services, Sunrise Senior Living, Discovery Senior Living, and Erickson Senior Living. The company also competes with major healthcare REITs like Ventas and Welltower for property acquisitions.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $3.16 billion in revenue over the past 12 months, Brookdale has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Sales Growth

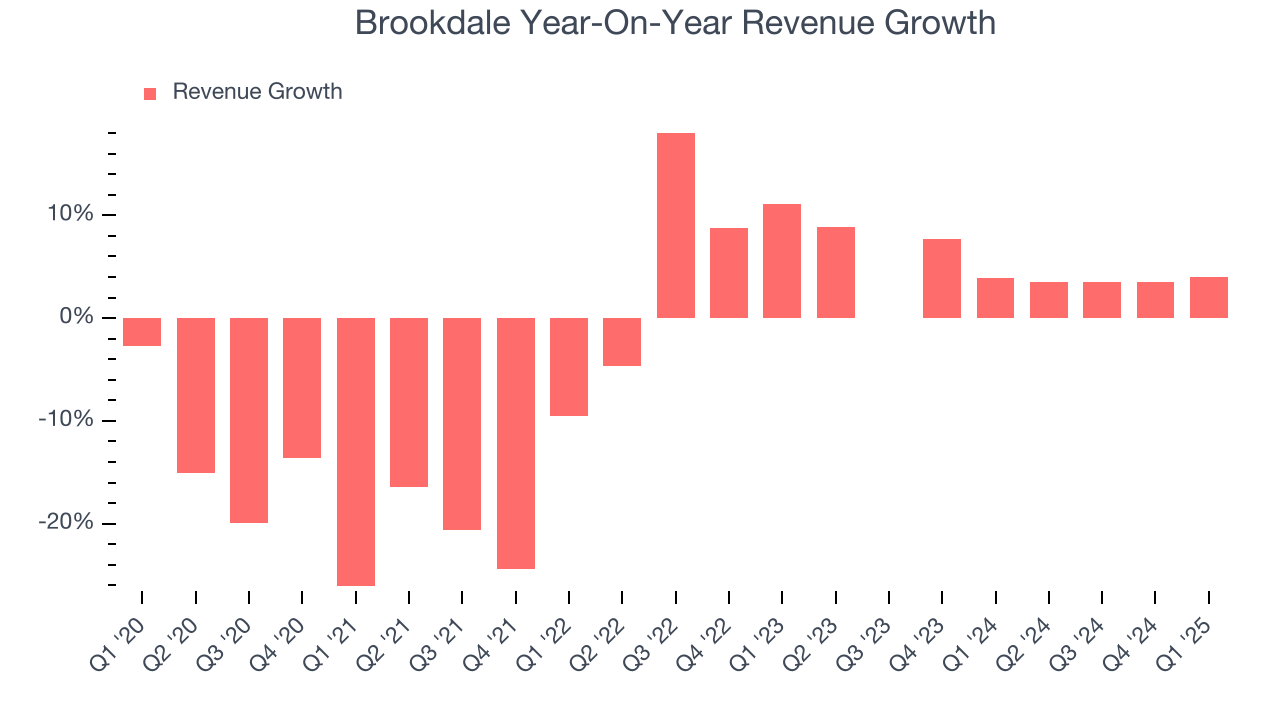

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Brookdale struggled to consistently generate demand over the last five years as its sales dropped at a 4.8% annual rate. This wasn’t a great result and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Brookdale’s annualized revenue growth of 4.3% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can better understand the company’s revenue dynamics by analyzing its most important segment, . Over the last two years, Brookdale’s revenue averaged 6.3% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, Brookdale grew its revenue by 4% year on year, and its $813.9 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Although Brookdale was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 1% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Brookdale’s operating margin rose by 6.6 percentage points over the last five years. This performance was mostly driven by its past improvements as the company’s margin was relatively unchanged on two-year basis.

This quarter, Brookdale generated an operating profit margin of 3.6%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Brookdale, its EPS declined by 27.1% annually over the last five years, more than its revenue. However, its operating margin actually expanded during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

We can take a deeper look into Brookdale’s earnings to better understand the drivers of its performance. A five-year view shows Brookdale has diluted its shareholders, growing its share count by 25%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Brookdale reported EPS at negative $0.28, down from negative $0.13 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Brookdale to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.03 will advance to negative $0.51.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Brookdale’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 3.7%. This means it lit $3.70 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Brookdale failed to improve its margin during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level.

Brookdale burned through $18.42 million of cash in Q1, equivalent to a negative 2.3% margin. The company’s cash burn slowed from $45.55 million of lost cash in the same quarter last year.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Brookdale’s five-year average ROIC was negative 0.9%, meaning management lost money while trying to expand the business. Investors are likely hoping for a change soon.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Brookdale’s ROIC has increased. This is a good sign, and we hope the company can continue improving.

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Brookdale burned through $7.94 million of cash over the last year, and its $5.60 billion of debt exceeds the $239.7 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Brookdale’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Brookdale until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

12. Key Takeaways from Brookdale’s Q1 Results

It was good to see Brookdale provide full-year EBITDA guidance that slightly beat analysts’ expectations. On the other hand, its EPS missed significantly and its revenue was in line with Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 5.4% to $6.42 immediately following the results.

13. Is Now The Time To Buy Brookdale?

Updated: June 28, 2025 at 12:07 AM EDT

When considering an investment in Brookdale, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Brookdale doesn’t pass our quality test. For starters, its revenue has declined over the last five years. And while its rising returns show management's prior bets are at least better than before, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its operating margins reveal poor profitability compared to other healthcare companies.

Brookdale’s EV-to-EBITDA ratio based on the next 12 months is 3.6x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $7.70 on the company (compared to the current share price of $6.90).