CVS Health (CVS)

We aren’t fans of CVS Health. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why CVS Health Is Not Exciting

With over 9,000 retail pharmacy locations serving as neighborhood health destinations across America, CVS Health (NYSE:CVS) operates retail pharmacies, provides pharmacy benefit management services, and offers health insurance through its Aetna subsidiary.

- Earnings per share fell by 2.9% annually over the last five years while its revenue grew, showing its incremental sales were much less profitable

- Responsiveness to unforeseen market trends is restricted due to its substandard adjusted operating profitability

- A silver lining is that its enormous revenue base of $379 billion gives it leverage over plan holders and advantageous reimbursement terms with healthcare providers

CVS Health’s quality doesn’t meet our expectations. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than CVS Health

CVS Health is trading at $60.80 per share, or 9.9x forward P/E. CVS Health’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. CVS Health (CVS) Research Report: Q1 CY2025 Update

Diversified healthcare company CVS Health (NYSE:CVS) beat Wall Street’s revenue expectations in Q1 CY2025, with sales up 7% year on year to $94.59 billion. Its non-GAAP profit of $2.25 per share was 34.6% above analysts’ consensus estimates.

CVS Health (CVS) Q1 CY2025 Highlights:

- Revenue: $94.59 billion vs analyst estimates of $93.18 billion (7% year-on-year growth, 1.5% beat)

- Adjusted EPS: $2.25 vs analyst estimates of $1.67 (34.6% beat)

- Adjusted EBITDA: $4.65 billion vs analyst estimates of $4.29 billion (4.9% margin, 8.5% beat)

- Management raised its full-year Adjusted EPS guidance to $6.10 at the midpoint, a 3.8% increase

- Operating Margin: 3.6%, in line with the same quarter last year

- Free Cash Flow Margin: 4%, similar to the same quarter last year

- Same-Store Sales rose 14.2% year on year (5.3% in the same quarter last year)

- Market Capitalization: $84.21 billion

Company Overview

With over 9,000 retail pharmacy locations serving as neighborhood health destinations across America, CVS Health (NYSE:CVS) operates retail pharmacies, provides pharmacy benefit management services, and offers health insurance through its Aetna subsidiary.

CVS Health operates through three main business segments: Health Care Benefits, Health Services, and Pharmacy & Consumer Wellness. The Health Care Benefits segment, which includes Aetna, serves more than 36 million people through various health insurance products including Medicare Advantage plans, employer-sponsored coverage, and Medicaid managed care. This segment competes with major health insurers like UnitedHealth and Cigna.

The Health Services segment provides pharmacy benefit management (PBM) solutions, helping clients design prescription drug plans, manage formularies, and control costs. It processes nearly 2 billion prescriptions annually and operates specialty pharmacies for complex medications. This segment also includes MinuteClinic, with more than 900 locations offering convenient care for minor illnesses and vaccinations, and newer acquisitions like Oak Street Health (primary care centers for Medicare patients) and Signify Health (in-home health evaluations).

The Pharmacy & Consumer Wellness segment is the most visible part of CVS Health's business, operating thousands of retail pharmacies that fill approximately 1.7 billion prescriptions annually and account for over 27% of all retail prescriptions in the U.S. These locations sell prescription medications and a wide range of health, wellness, and general merchandise products. This segment also includes Omnicare, which provides pharmacy services to long-term care facilities.

CVS Health's integrated model allows it to serve customers across the healthcare spectrum. For example, a customer might have Aetna insurance, get prescriptions filled at a CVS pharmacy, receive care at MinuteClinic, and benefit from cost management through the company's PBM services. The company leverages its vast physical footprint and growing digital capabilities to deliver care when and where consumers need it, while using data and analytics to improve health outcomes and reduce costs.

4. Health Insurance Providers

Upfront premiums collected by health insurers lead to reliable revenue, but profitability ultimately depends on accurate risk assessments and the ability to control medical costs. Health insurers are also highly sensitive to regulatory changes and economic conditions such as unemployment. Going forward, the industry faces tailwinds from an aging population, increasing demand for personalized healthcare services, and advancements in data analytics to improve cost management. However, continued regulatory scrutiny on pricing practices, the potential for government-led reforms such as expanded public healthcare options, and inflation in medical costs could add volatility to margins. One big debate among investors is the long-term impact of AI and whether it will help underwriting, fraud detection, and claims processing or whether it may wade into ethical grey areas like reinforcing biases and widening disparities in medical care.

CVS Health competes with Walgreens Boots Alliance (NASDAQ:WBA) and Rite Aid (NYSE:RAD) in retail pharmacy, UnitedHealth Group's Optum Rx (NYSE:UNH) and Cigna's Express Scripts (NYSE:CI) in pharmacy benefit management, and major health insurers like UnitedHealth, Cigna, Humana (NYSE:HUM), and Elevance Health (NYSE:ELV) in health insurance.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $379 billion in revenue over the past 12 months, CVS Health is one of the most scaled enterprises in healthcare. This is particularly important because health insurance providers companies are volume-driven businesses due to their low margins.

6. Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, CVS Health grew its sales at a decent 7.7% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. CVS Health’s annualized revenue growth of 7% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can dig further into the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, CVS Health’s same-store sales averaged 10.3% year-on-year growth. Because this number is better than its revenue growth, we can see its sales from existing locations are performing better than its sales from new locations.

This quarter, CVS Health reported year-on-year revenue growth of 7%, and its $94.59 billion of revenue exceeded Wall Street’s estimates by 1.5%.

Looking ahead, sell-side analysts expect revenue to grow 3.7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

7. Adjusted Operating Margin

CVS Health was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 5% was weak for a healthcare business.

Analyzing the trend in its profitability, CVS Health’s adjusted operating margin decreased by 2.4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 1.8 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, CVS Health generated an adjusted operating profit margin of 4.8%, up 1.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

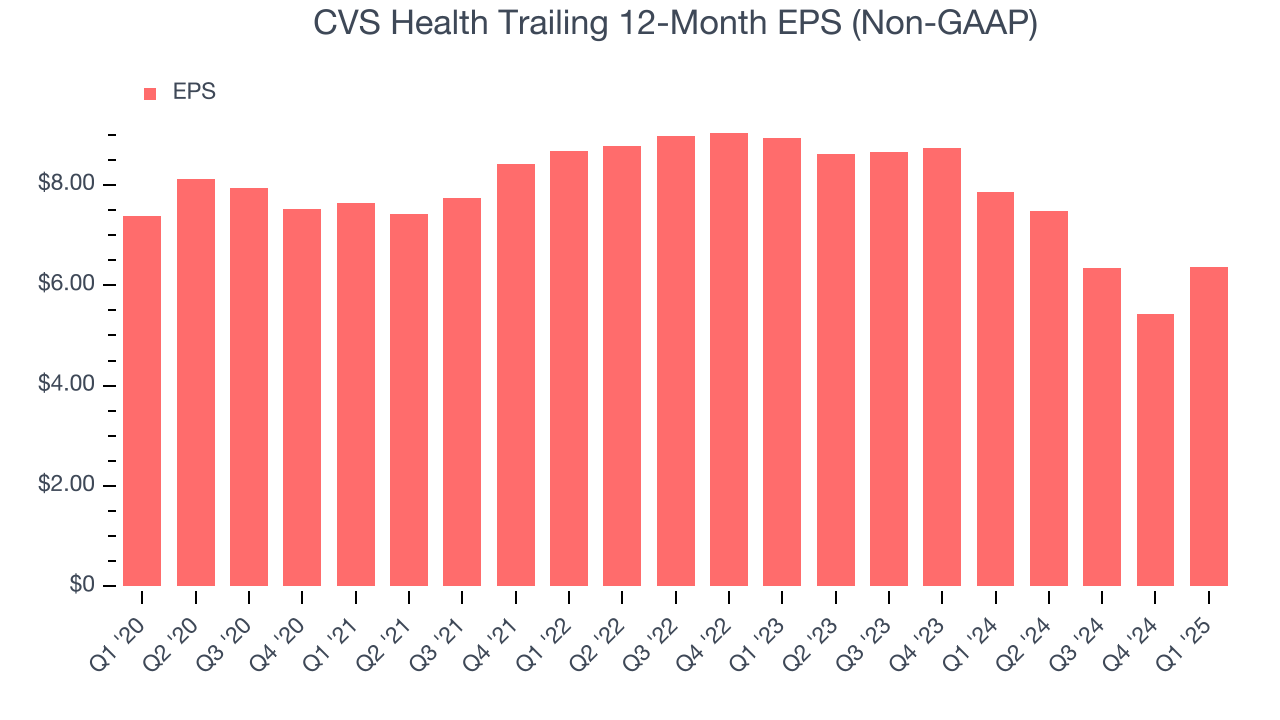

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for CVS Health, its EPS declined by 2.9% annually over the last five years while its revenue grew by 7.7%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of CVS Health’s earnings can give us a better understanding of its performance. As we mentioned earlier, CVS Health’s adjusted operating margin improved this quarter but declined by 2.4 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, CVS Health reported EPS at $2.25, up from $1.31 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects CVS Health’s full-year EPS of $6.36 to shrink by 3.1%.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

CVS Health has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.7%, subpar for a healthcare business.

Taking a step back, we can see that CVS Health’s margin dropped by 3.2 percentage points during that time. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s in the middle of an investment cycle.

CVS Health’s free cash flow clocked in at $3.81 billion in Q1, equivalent to a 4% margin. This cash profitability was in line with the comparable period last year and its five-year average.

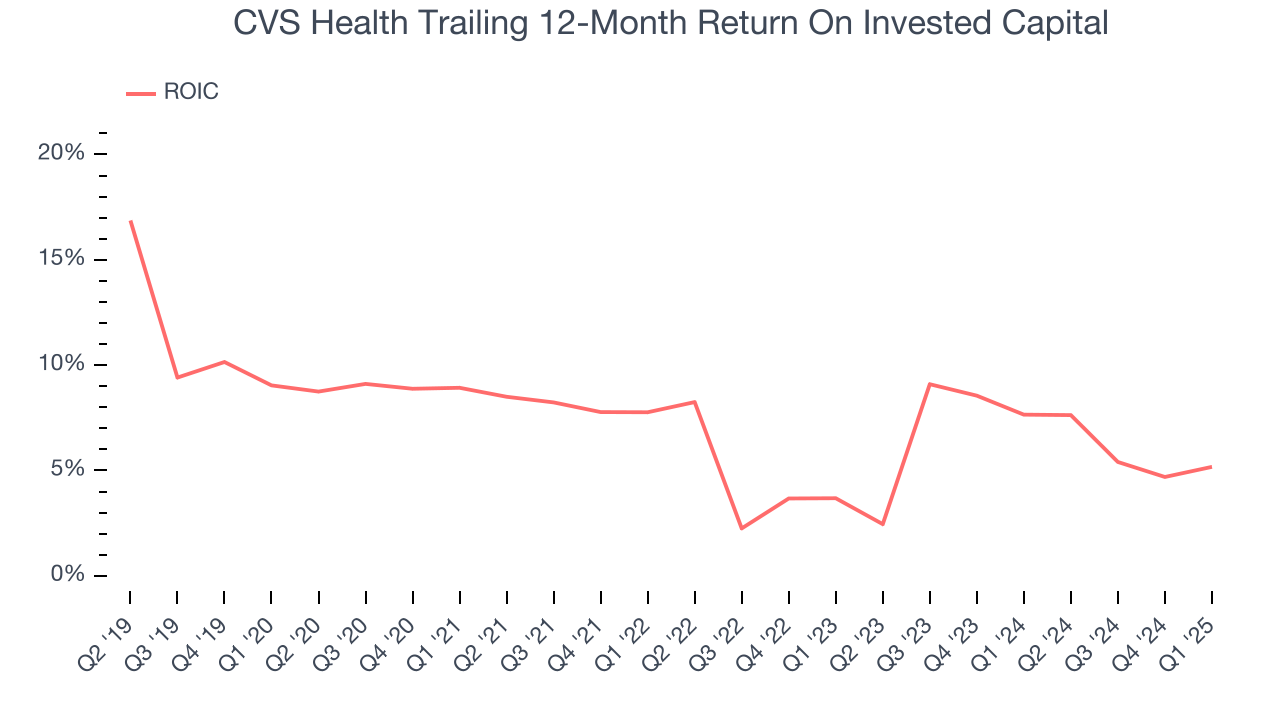

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

CVS Health historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.6%, somewhat low compared to the best healthcare companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, CVS Health’s ROIC averaged 1.9 percentage point decreases each year. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

CVS Health reported $12.65 billion of cash and $76.8 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $15.62 billion of EBITDA over the last 12 months, we view CVS Health’s 4.1× net-debt-to-EBITDA ratio as safe. We also see its $242 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from CVS Health’s Q1 Results

This was a 'beat and raise' quarter. We were impressed by how significantly CVS Health blew past analysts’ same-store sales expectations this quarter. We were also excited its EPS outperformed Wall Street’s estimates by a wide margin. Looking ahead, the company raised its full-year EPS guidance. Zooming out, we think this quarter featured some important positives. The stock traded up 8.9% to $72.61 immediately after reporting.

13. Is Now The Time To Buy CVS Health?

Updated: May 26, 2025 at 11:37 PM EDT

Before deciding whether to buy CVS Health or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

CVS Health doesn’t top our investment wishlist, but we understand that it’s not a bad business. First off, its revenue growth was decent over the last five years. And while CVS Health’s declining EPS over the last five years makes it a less attractive asset to the public markets, its scale gives it meaningful leverage when negotiating reimbursement rates.

CVS Health’s P/E ratio based on the next 12 months is 9.9x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $79.29 on the company (compared to the current share price of $60.80).

Enjoyed this research report? Then you will absolutely love StockStory Edge.

Our team provides you with in-depth research on more than 1,100 stocks including many small and mid-caps nobody else covers, helping you understand not only what to buy but also what to avoid.

Did you know that StockStory’s High Quality stocks generated a market-beating return of 183% from March 31, 2020 to March 31, 2025 vs an 117% return for the market? We achieve this consistent outperformance by blending AI-powered analysis with the experitize of our expert analysts to identify opportunities overlooked by the market.

There is a good chance you right now qualify for our new user introductory discount. Sign up now and get access to market-beating stocks picks, critical why stocks move alerts, earnings call insights and so much more.

And if it isn't for you? No worries, our annual plan is backed by 14-day money-back guarantee, 100% risk-free.

PS. We are so confident you will love StockStory Edge we have awarded you a limited 7-day test drive of our platform (Stock Picks are for our paying members only but you can try everything else). To get the most out of it check out our timely selection of High Quality stocks, and then sign up for our timely Why It Moves alerts and earnings results updates by adding companies to your watchlist. But hurry, your trial and discount expire soon.