GoDaddy (GDDY)

GoDaddy doesn’t excite us. Its weak revenue growth and gross margin show it not only lacks demand but also decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why We Think GoDaddy Will Underperform

Founded by Bob Parsons after selling his first company to Intuit, GoDaddy (NYSE:GDDY) provides small and mid-sized businesses with the ability to buy a web domain and tools to create and manage a website.

- Sales trends were unexciting over the last three years as its 6% annual growth was well below the typical software company

- Steep infrastructure costs and weaker unit economics for a software company are reflected in its low gross margin of 64%

- On the plus side, its successful business model is illustrated by its impressive operating margin, and it turbocharged its profits by achieving some fixed cost leverage

GoDaddy is in the doghouse. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than GoDaddy

GoDaddy is trading at $174.87 per share, or 5.1x forward price-to-sales. GoDaddy’s valuation may seem like a bargain, especially when stacked up against other software companies. We remind you that you often get what you pay for, though.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. GoDaddy (GDDY) Research Report: Q1 CY2025 Update

Domain registrar and web services company GoDaddy (NYSE:GDDY) reported Q1 CY2025 results topping the market’s revenue expectations, with sales up 7.7% year on year to $1.19 billion. The company expects next quarter’s revenue to be around $1.21 billion, close to analysts’ estimates. Its GAAP profit of $1.51 per share was 9.9% above analysts’ consensus estimates.

GoDaddy (GDDY) Q1 CY2025 Highlights:

- Revenue: $1.19 billion vs analyst estimates of $1.19 billion (7.7% year-on-year growth, 0.6% beat)

- EPS (GAAP): $1.51 vs analyst estimates of $1.37 (9.9% beat)

- Adjusted EBITDA: $364.4 million vs analyst estimates of $357.5 million (30.5% margin, 1.9% beat)

- The company reconfirmed its revenue guidance for the full year of $4.9 billion at the midpoint

- Operating Margin: 20.7%, up from 15.9% in the same quarter last year

- Free Cash Flow Margin: 34.4%, up from 28.7% in the previous quarter

- Customers: 20.48 million, down from 20.51 million in the previous quarter

- Annual Recurring Revenue: $4.05 billion at quarter end, up 7.5% year on year

- Billings: $1.35 billion at quarter end

- Market Capitalization: $26.01 billion

Company Overview

Founded by Bob Parsons after selling his first company to Intuit, GoDaddy (NYSE:GDDY) provides small and mid-sized businesses with the ability to buy a web domain and tools to create and manage a website.

Successfully setting up an online store is difficult for most small business owners. GoDaddy offers most of the e-commerce functionalities to simplify the entire process of starting and maintaining an online business.

By making it easy for even non-technical users to set up a fully functioning website within a short period, GoDaddy helps its customers to focus their time on their primary business function.

For example, you don’t need computers to make food, however, restaurants rely on computers and websites to sell and deliver food to customers. For a small restaurant business, GoDaddy starts by providing a fitting domain name. It then provides all the tools to host, build, and manage a website. It also integrates with third-party applications to provide payment, marketing, and other e-commerce features.

GoDaddy was founded when the sale and management of domain names were popular and lucrative. As more companies moved into the domain name business, GoDaddy expanded into the e-commerce space by offering more robust website services to stay competitive.

4. E-commerce Software

While e-commerce has been around for over two decades and enjoyed meaningful growth, its overall penetration of retail still remains low. Only around $1 in every $5 spent on retail purchases comes from digital orders, leaving over 80% of the retail market still ripe for online disruption. It is these large swathes of the retail where e-commerce has not yet taken hold that drives the demand for various e-commerce software solutions.

GoDaddy faces competition from Automattic, Shopify (NYSE: SHOP), Squarespace (NYSE: SQSP), and Wix (NASDAQ: WIX).

5. Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, GoDaddy grew its sales at a weak 6% compounded annual growth rate. This fell short of our benchmark for the software sector and is a tough starting point for our analysis.

This quarter, GoDaddy reported year-on-year revenue growth of 7.7%, and its $1.19 billion of revenue exceeded Wall Street’s estimates by 0.6%. Company management is currently guiding for a 7.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.8% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and indicates its newer products and services will not catalyze better top-line performance yet.

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

GoDaddy’s ARR came in at $4.05 billion in Q1, and over the last four quarters, its growth was underwhelming as it averaged 8% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in securing longer-term commitments.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for GoDaddy to acquire new customers as its CAC payback period checked in at 136.7 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

8. Gross Margin & Pricing Power

For software companies like GoDaddy, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

GoDaddy’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 64% gross margin over the last year. That means GoDaddy paid its providers a lot of money ($36.02 for every $100 in revenue) to run its business.

This quarter, GoDaddy’s gross profit margin was 63.1%, in line with the same quarter last year. On a wider time horizon, GoDaddy’s full-year margin has been trending up over the past 12 months, increasing by 1 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

9. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

GoDaddy has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 20.7%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, GoDaddy’s operating margin rose by 5.6 percentage points over the last year, as its sales growth gave it operating leverage.

This quarter, GoDaddy generated an operating profit margin of 20.7%, up 4.8 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

GoDaddy has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 30.9% over the last year.

GoDaddy’s free cash flow clocked in at $411.3 million in Q1, equivalent to a 34.4% margin. This result was good as its margin was 4.9 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts predict GoDaddy’s cash conversion will slightly improve. Their consensus estimates imply its free cash flow margin of 30.9% for the last 12 months will increase to 33.3%, it options for capital deployment (investments, share buybacks, etc.).

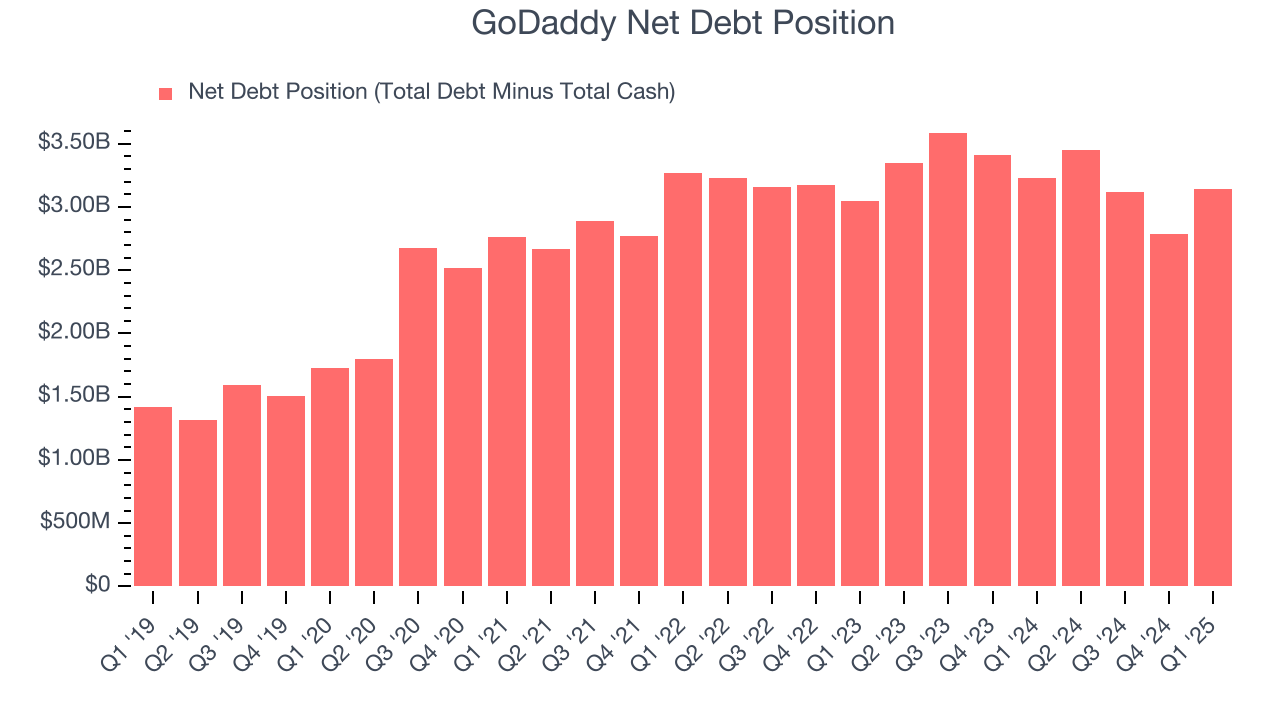

11. Balance Sheet Assessment

GoDaddy reported $719.4 million of cash and $3.87 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.45 billion of EBITDA over the last 12 months, we view GoDaddy’s 2.2× net-debt-to-EBITDA ratio as safe. We also see its $154.2 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from GoDaddy’s Q1 Results

We were impressed by how significantly GoDaddy blew past analysts’ bookings expectations this quarter. We were also happy its revenue, EPS, and EBITDA outperformed Wall Street’s estimates. On the other hand, its annual recurring revenue missed. Zooming out, we think this was a decent quarter featuring some areas of strength but also some blemishes. The market seemed to be hoping for more, and the stock traded down 6.5% to $180 immediately after reporting.

13. Is Now The Time To Buy GoDaddy?

Updated: June 23, 2025 at 10:15 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in GoDaddy.

GoDaddy isn’t a terrible business, but it doesn’t pass our bar. For starters, its revenue growth was weak over the last three years. And while its bountiful generation of free cash flow empowers it to invest in growth initiatives, the downside is its gross margins show its business model is much less lucrative than other companies. On top of that, its ARR has disappointed and shows the company is having difficulty retaining customers and their spending.

GoDaddy’s price-to-sales ratio based on the next 12 months is 5.2x. Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $210.78 on the company (compared to the current share price of $177.99).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.