Tri Pointe Homes (TPH)

We wouldn’t recommend Tri Pointe Homes. Its weak sales growth and declining returns on capital show its demand and profits are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Tri Pointe Homes Will Underperform

Established in 2009 in California, Tri Pointe Homes (NYSE:TPH) is a United States homebuilder recognized for its innovative and sustainable approach to creating premium, life-enhancing homes.

- Customers postponed purchases of its products and services this cycle as its revenue declined by 1.1% annually over the last two years

- Sales were less profitable over the last two years as its earnings per share fell by 9.5% annually, worse than its revenue declines

- Projected sales decline of 19% over the next 12 months indicates demand will continue deteriorating

Tri Pointe Homes doesn’t fulfill our quality requirements. Better stocks can be found in the market.

Why There Are Better Opportunities Than Tri Pointe Homes

Tri Pointe Homes’s stock price of $31.10 implies a valuation ratio of 10x forward P/E. Tri Pointe Homes’s multiple may seem like a great deal among industrials peers, but we think there are valid reasons why it’s this cheap.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Tri Pointe Homes (TPH) Research Report: Q1 CY2025 Update

Homebuilder Tri Pointe Homes (NYSE:TPH) reported Q1 CY2025 results exceeding the market’s revenue expectations, but sales fell by 23% year on year to $723.4 million. Its GAAP profit of $0.70 per share was 42.9% above analysts’ consensus estimates.

Tri Pointe Homes (TPH) Q1 CY2025 Highlights:

- Revenue: $723.4 million vs analyst estimates of $712.5 million (23% year-on-year decline, 1.5% beat)

- EPS (GAAP): $0.70 vs analyst estimates of $0.49 (42.9% beat)

- Adjusted EBITDA: $125.7 million vs analyst estimates of $92.9 million (17.4% margin, 35.3% beat)

- Operating Margin: 10%, down from 12.3% in the same quarter last year

- Backlog: $1.31 billion at quarter end, down 33% year on year

- Market Capitalization: $2.83 billion

Company Overview

Established in 2009 in California, Tri Pointe Homes (NYSE:TPH) is a United States homebuilder recognized for its innovative and sustainable approach to creating premium, life-enhancing homes.

Tri Pointe Homes was founded in 2009 and is a leading homebuilder and real estate developer in the United States, offering a range of innovative single-family attached and detached homes across multiple markets.

Tri Pointe has grown from a Southern California fee homebuilder into a national player, capitalizing on high-demand markets with favorable population and employment growth. The company's strategy focuses on acquiring attractive land positions while reducing risk and expanding its market presence through organic growth and strategic acquisitions.

The company offers a variety of product offerings, from entry-level to luxury homes, allowing it to serve a broad spectrum of homebuyers and adapt to changing market conditions. In addition to homebuilding, Tri Pointe offers complementary financial services through its Tri Pointe Solutions division, which includes mortgage financing, title and escrow services, and property and casualty insurance agency operations. These services enhance the overall homebuying experience for customers and provide additional revenue streams for the company.

Tri Pointe emphasizes quality control, customer service, and warranty programs to ensure homebuyer satisfaction.Tri Pointe Homes generates revenue primarily through individual home sales, with buyers typically providing a small deposit upfront and the bulk of payment at closing. The company recognizes most revenue upon home completion and transfer of ownership, rather than using long-term contracts or milestone-based payments.

4. Home Builders

Traditionally, homebuilders have built competitive advantages with economies of scale that lead to advantaged purchasing and brand recognition among consumers. Aesthetic trends have always been important in the space, but more recently, energy efficiency and conservation are driving innovation. However, these companies are still at the whim of the macro, specifically interest rates that heavily impact new and existing home sales. In fact, homebuilders are one of the most cyclical subsectors within industrials.

Tri Pointe Homes’ main competitors include Lennar Corporation (NYSE:LEN), D.R. Horton (NYSE:DHI), PulteGroup (NYSE:PHM), and Toll Brothers (NYSE:TOL).

5. Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Tri Pointe Homes grew its sales at a mediocre 6.1% compounded annual growth rate. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Tri Pointe Homes’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.3% annually.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Tri Pointe Homes’s backlog reached $1.31 billion in the latest quarter and averaged 6.9% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, Tri Pointe Homes’s revenue fell by 23% year on year to $723.4 million but beat Wall Street’s estimates by 1.5%.

Looking ahead, sell-side analysts expect revenue to decline by 11.6% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

6. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

Tri Pointe Homes has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 24.6% gross margin over the last five years. Said differently, Tri Pointe Homes had to pay a chunky $75.44 to its suppliers for every $100 in revenue.

In Q1, Tri Pointe Homes produced a 24% gross profit margin, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

Tri Pointe Homes has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 14.4%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Tri Pointe Homes’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Tri Pointe Homes generated an operating profit margin of 10%, down 2.4 percentage points year on year. Since Tri Pointe Homes’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Tri Pointe Homes’s EPS grew at an astounding 21.3% compounded annual growth rate over the last five years, higher than its 6.1% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t expand.

We can take a deeper look into Tri Pointe Homes’s earnings quality to better understand the drivers of its performance. A five-year view shows that Tri Pointe Homes has repurchased its stock, shrinking its share count by 31.8%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Tri Pointe Homes, its two-year annual EPS declines of 9.6% mark a reversal from its (seemingly) healthy five-year trend. We hope Tri Pointe Homes can return to earnings growth in the future.

In Q1, Tri Pointe Homes reported EPS at $0.70, down from $1.03 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Tri Pointe Homes’s full-year EPS of $4.50 to shrink by 31.1%.

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Tri Pointe Homes has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 12% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Tri Pointe Homes’s margin dropped by 9.8 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

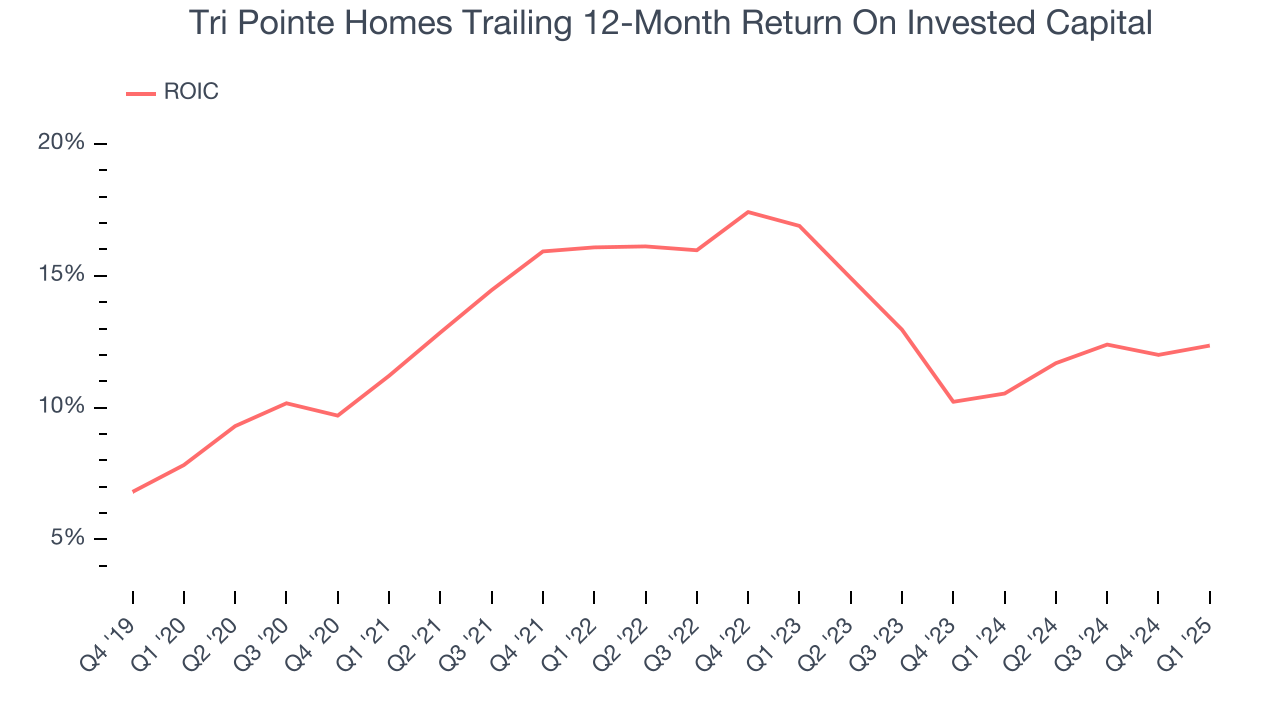

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Tri Pointe Homes hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked. Its five-year average ROIC was 13.4%, higher than most industrials businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Tri Pointe Homes’s ROIC averaged 2.2 percentage point decreases each year. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

Tri Pointe Homes reported $812.9 million of cash and $914.6 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $755.1 million of EBITDA over the last 12 months, we view Tri Pointe Homes’s 0.1× net-debt-to-EBITDA ratio as safe. We also see its $0 of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Tri Pointe Homes’s Q1 Results

We were impressed by how significantly Tri Pointe Homes blew past analysts’ EPS expectations this quarter. On the other hand, its backlog missed, and this shortfall in a key leading indicator of future revenue seems to be weighing on shares. The stock traded down 4.3% to $29.51 immediately following the results.

13. Is Now The Time To Buy Tri Pointe Homes?

Updated: June 11, 2025 at 11:52 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Tri Pointe Homes, you should also grasp the company’s longer-term business quality and valuation.

We see the value of companies helping their customers, but in the case of Tri Pointe Homes, we’re out. To begin with, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. And while its astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its projected EPS for the next year is lacking. On top of that, its cash profitability fell over the last five years.

Tri Pointe Homes’s P/E ratio based on the next 12 months is 10x. This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $39.17 on the company (compared to the current share price of $31.10).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.