Appian (APPN)

We’re wary of Appian. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why Appian Is Not Exciting

Founded by Matt Calkins and his three friends out of an apartment in Northern Virginia, Appian (NASDAQ:APPN) sells a software platform that lets its users build applications without using much code, allowing them to create new software more quickly.

- Long payback periods on sales and marketing expenses limit customer growth and signal the company operates in a highly competitive environment

- Low free cash flow margin gives it little breathing room, constraining its ability to self-fund growth or return capital to shareholders

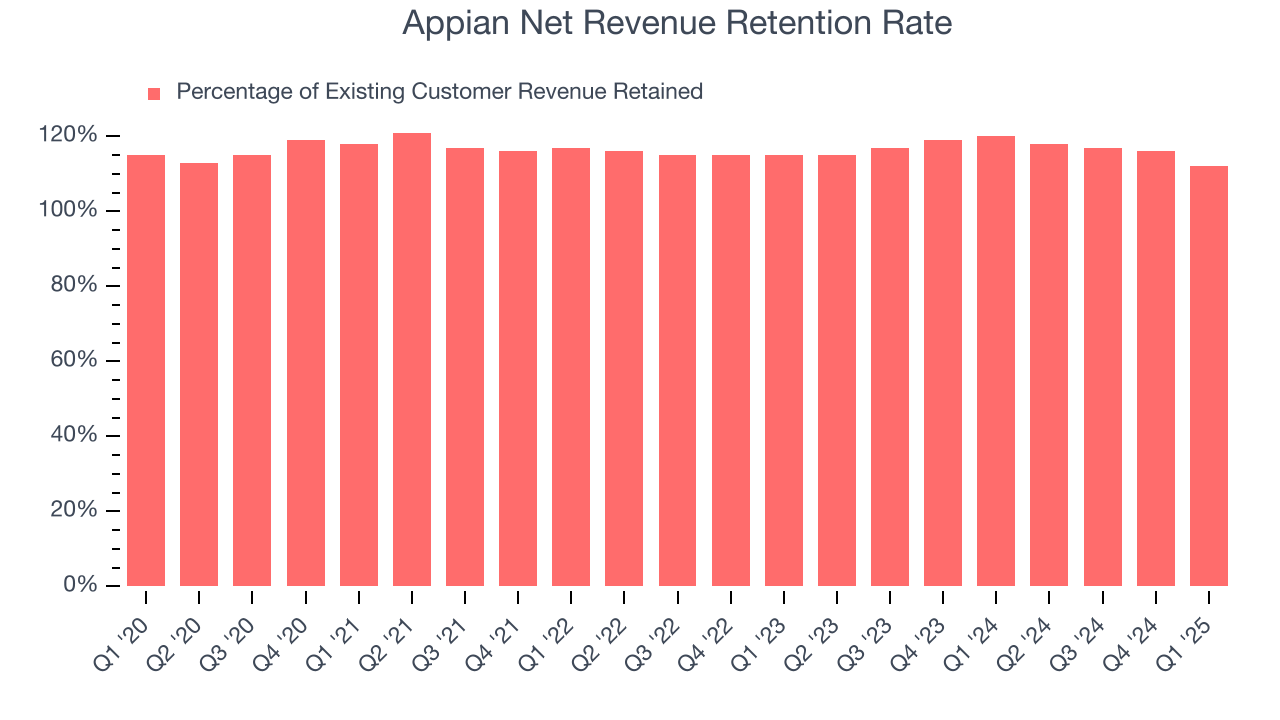

- On the plus side, its customers use its software daily and increase their spending every year, as seen in its 116% net revenue retention rate

Appian doesn’t meet our quality standards. There are superior opportunities elsewhere.

Why There Are Better Opportunities Than Appian

Appian’s stock price of $31.31 implies a valuation ratio of 3.3x forward price-to-sales. Appian’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Appian (APPN) Research Report: Q1 CY2025 Update

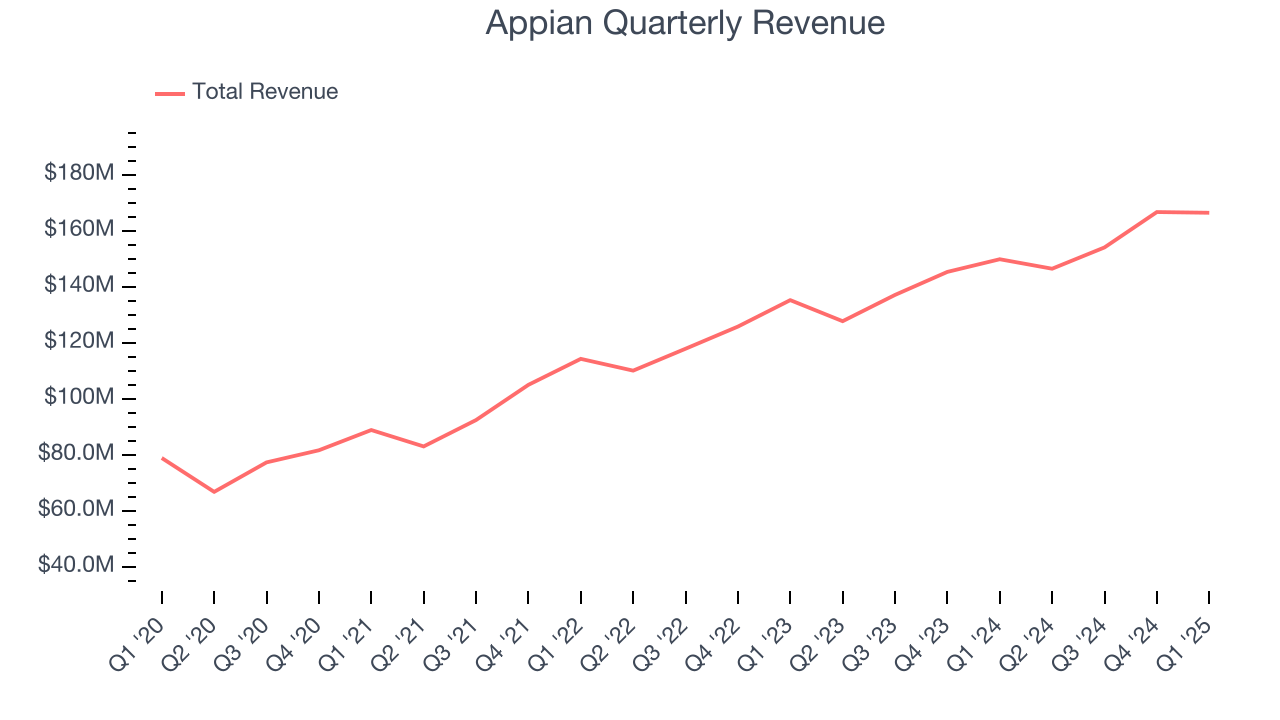

Low code software development platform provider Appian (Nasdaq: APPN) announced better-than-expected revenue in Q1 CY2025, with sales up 11.1% year on year to $166.4 million. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $160 million was less impressive, coming in 0.8% below expectations. Its non-GAAP profit of $0.13 per share was significantly above analysts’ consensus estimates.

Appian (APPN) Q1 CY2025 Highlights:

- Revenue: $166.4 million vs analyst estimates of $163.2 million (11.1% year-on-year growth, 2% beat)

- Adjusted EPS: $0.13 vs analyst estimates of $0.03 (significant beat)

- Adjusted EBITDA: $16.76 million vs analyst estimates of $9.19 million (10.1% margin, 82.5% beat)

- The company slightly lifted its revenue guidance for the full year to $684 million at the midpoint from $682 million

- Management raised its full-year Adjusted EPS guidance to $0.22 at the midpoint, a 12.8% increase

- EBITDA guidance for the full year is $43 million at the midpoint, above analyst estimates of $39.14 million

- Operating Margin: -0.5%, up from -13% in the same quarter last year

- Free Cash Flow Margin: 26.6%, up from 8% in the previous quarter

- Net Revenue Retention Rate: 112%, down from 116% in the previous quarter

- Market Capitalization: $2.26 billion

Company Overview

Founded by Matt Calkins and his three friends out of an apartment in Northern Virginia, Appian (NASDAQ:APPN) sells a software platform that lets its users build applications without using much code, allowing them to create new software more quickly.

By empowering existing teams within specialist organisations, Appian lets its diverse customers, from banks to wind farms, build the exact software they need. This might mean creating new interfaces for tellers, or building a process for acquiring and managing wind farm insurance. By making software development easier with pre-existing segments of code, Appian's customers can build and deploy new functionality far more quickly, and potentially at lower cost, than if they had to hire more team members to build it without Appian.

Appian was started by four young friends, including long-serving CEO Matt Calkins who quit his job before settling on a business plan. It wasn't until a few years later that the company began to focus on business process management, helping companies become more efficient. Today, Appian can potentially allow any employee to develop the specific custom software that their business needs.

4. Automation Software

The whole purpose of software is to automate tasks to increase productivity. Today, innovative new software techniques, often involving AI and machine learning, are finally allowing automation that has graduated from simple one- or two-step workflows to more complex processes integral to enterprises. The result is surging demand for modern automation software.

Other providers of low code software include Pegasystems (NASDAQ:PEGA), IBM (NYSE:IBM), and Oracle (NYSE:ORCL).

5. Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, Appian grew its sales at a 17.1% annual rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

This quarter, Appian reported year-on-year revenue growth of 11.1%, and its $166.4 million of revenue exceeded Wall Street’s estimates by 2%. Company management is currently guiding for a 9.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates its products and services will face some demand challenges.

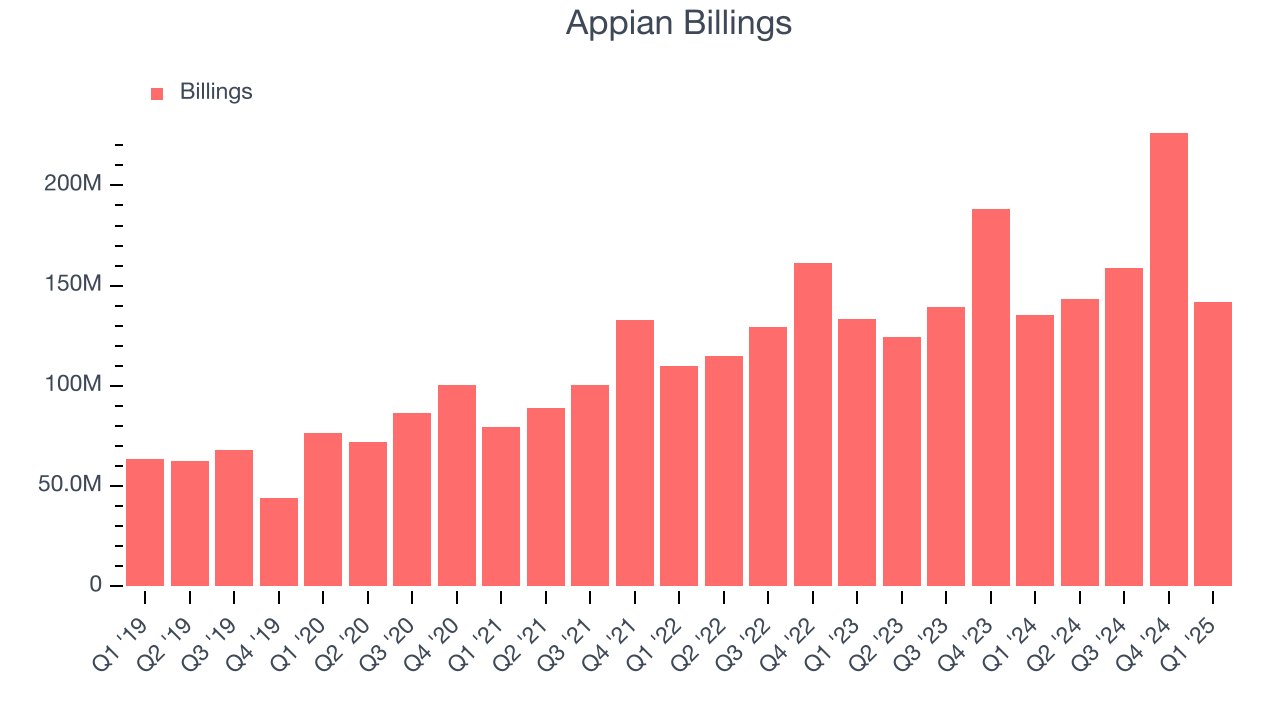

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Appian’s billings punched in at $141.7 million in Q1, and over the last four quarters, its growth slightly outpaced the sector as it averaged 13.5% year-on-year increases. This performance aligned with its total sales growth and shows the company is successfully converting sales into cash. Its growth also enhances liquidity and provides a solid foundation for future investments.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Appian’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Appian’s products and its peers.

8. Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Appian’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 116% in Q1. This means Appian would’ve grown its revenue by 15.7% even if it didn’t win any new customers over the last 12 months.

Despite falling over the last year, Appian still has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

9. Gross Margin & Pricing Power

For software companies like Appian, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Appian’s robust unit economics are better than the broader software industry, an output of its asset-lite business model and pricing power. They also enable the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an excellent 76.4% gross margin over the last year. Said differently, roughly $76.37 was left to spend on selling, marketing, and R&D for every $100 in revenue.

In Q1, Appian produced a 76.6% gross profit margin, up 2 percentage points year on year. Appian’s full-year margin has also been trending up over the past 12 months, increasing by 2.3 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

10. Operating Margin

Although Appian broke even this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 6.7% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Appian reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Over the last year, Appian’s expanding sales gave it operating leverage as its margin rose by 9.8 percentage points. Still, it will take much more for the company to reach long-term profitability.

Appian’s operating margin was negative 0.5% this quarter. The company's consistent lack of profits raise a flag.

11. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Appian has shown weak cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.8%, subpar for a software business.

Appian’s free cash flow clocked in at $44.32 million in Q1, equivalent to a 26.6% margin. This result was good as its margin was 15.5 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts’ consensus estimates show they’re expecting Appian’s free cash flow margin of 4.8% for the last 12 months to remain the same.

12. Balance Sheet Assessment

Appian reported $199.7 million of cash and $302.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $38.34 million of EBITDA over the last 12 months, we view Appian’s 2.7× net-debt-to-EBITDA ratio as safe. We also see its $12.62 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Appian’s Q1 Results

We liked that revenue beat and were impressed by how significantly Appian blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. On the other hand, its revenue guidance for next quarter fell slightly short of Wall Street’s estimates. Zooming out, we think this was still a decent quarter. The stock traded up 7.1% to $32.55 immediately following the results.

14. Is Now The Time To Buy Appian?

Updated: May 29, 2025 at 10:14 PM EDT

Are you wondering whether to buy Appian or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Appian isn’t a terrible business, but it doesn’t pass our bar. First off, its revenue growth was a little slower over the last three years, and analysts expect its demand to deteriorate over the next 12 months. And while its expanding operating margin shows it’s becoming more efficient at building and selling its software, the downside is its customer acquisition is less efficient than many comparable companies. On top of that, its low free cash flow margins give it little breathing room.

Appian’s price-to-sales ratio based on the next 12 months is 3.3x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $34.83 on the company (compared to the current share price of $31.31).

Enjoyed this research report? Then you will absolutely love StockStory Edge.

StockStory Edge provides you with in-depth research on more than 1,100 stocks including many that fly under-the-radar, helping you understand not only what to buy but also what to avoid.

Did you know that StockStory High Quality stocks generated a market-beating return of 183% from March 31, 2020 to March 31, 2025 vs an 117% return for the market? We achieve this outperformance by blending AI-powered analysis with the experitize of our analysts to identify opportunities overlooked by the market.