Netflix (NFLX)

We’d invest in Netflix. It’s not only a cash cow but also has increased its profitability, showing its fundamentals are improving.― StockStory Analyst Team

1. News

2. Summary

Why We Like Netflix

Launched by Reed Hastings as a DVD mail rental company until its famous pivot to streaming in 2007, Netflix (NASDAQ: NFLX) is a pioneering streaming content platform.

- Healthy EBITDA margin shows it’s a well-run company with efficient processes, and its operating leverage amplified its profits over the last few years

- Word-of-mouth marketing drives organic user growth, eliminating the need for costly advertising campaigns

- Additional sales over the last three years increased its profitability as the 24.3% annual growth in its earnings per share outpaced its revenue

Netflix is a standout company. This is one of the finest consumer internet stocks in our coverage.

Is Now The Time To Buy Netflix?

Netflix’s stock price of $1,220 implies a valuation ratio of 37.8x forward EV/EBITDA. There’s no arguing the market has lofty expectations given its premium multiple.

Do you like the business model and believe in the company’s future? If so, you can own a smaller position, as our work shows that high-quality companies outperform the market over a multi-year period regardless of valuation at entry.

3. Netflix (NFLX) Research Report: Q1 CY2025 Update

Streaming video giant Netflix (NASDAQ: NFLX) met Wall Street’s revenue expectations in Q1 CY2025, with sales up 12.5% year on year to $10.54 billion. The company expects next quarter’s revenue to be around $11.04 billion, slightly above analysts’ estimates. Its GAAP profit of $6.61 per share was 16.8% above analysts’ consensus estimates.

Netflix (NFLX) Q1 CY2025 Highlights:

- Revenue: $10.54 billion vs analyst estimates of $10.51 billion (12.5% year-on-year growth, in line)

- EPS (GAAP): $6.61 vs analyst estimates of $5.66 (16.8% beat)

- The company reconfirmed its revenue guidance for the full year of $44 billion at the midpoint

- EPS (GAAP) guidance for Q2 CY2025 is $7.03 at the midpoint, beating analyst estimates by 12.7%

- Operating Margin: 31.7%, up from 28.1% in the same quarter last year

- Free Cash Flow Margin: 25.2%, up from 13.5% in the previous quarter

- Market Capitalization: $411.3 billion

Company Overview

Launched by Reed Hastings as a DVD mail rental company until its famous pivot to streaming in 2007, Netflix (NASDAQ: NFLX) is a pioneering streaming content platform.

Netflix has a large and ever growing library of TV shows, movies, documentaries, and children’s programming. The company is known for its innovative approach to content delivery. For its first 10 years, that meant DVD rentals by mail with no return date. It launched streaming in 2007, which used customer data to surface programming that users might be interested in.

In 2013, the company began producing its own programming, weaning itself off of relying entirely on other company’s content. Hit shows such as "Stranger Things" and "The Crown" drew in audiences and kept them loyal to the platform. Today, Netflix generates revenue through its subscription-based model as well as an ad-supported one, with different plans at various price points.

For consumers, Netflix upended the traditional model of consuming content, flipping the paradigm from “appointment viewing” to a more customer centric “on demand viewing” Netflix’s granular viewing data also fundamentally altered what type of content was produced, stratifying what was once a handful of genres into dozens of niches that are able to find audiences in a sea of viewers. These innovations have been mimicked by many streaming services, and have become a quasi-standard of content consumption today.

4. Consumer Subscription

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

Netflix (NASDAQ:NFLX) competes with a range of streaming content rivals, from Amazon (NASDAQ: AMZN) and Disney (NYSE:DIS) to Paramount (NASDAQ:PARA) and Warner Bros Discovery (NASDAQ:WBD).

5. Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, Netflix grew its sales at a mediocre 9.7% compounded annual growth rate. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Netflix.

This quarter, Netflix’s year-on-year revenue growth was 12.5%, and its $10.54 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 15.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.7% over the next 12 months, an acceleration versus the last three years. This projection is particularly healthy for a company of its scale and suggests its newer products and services will spur better top-line performance.

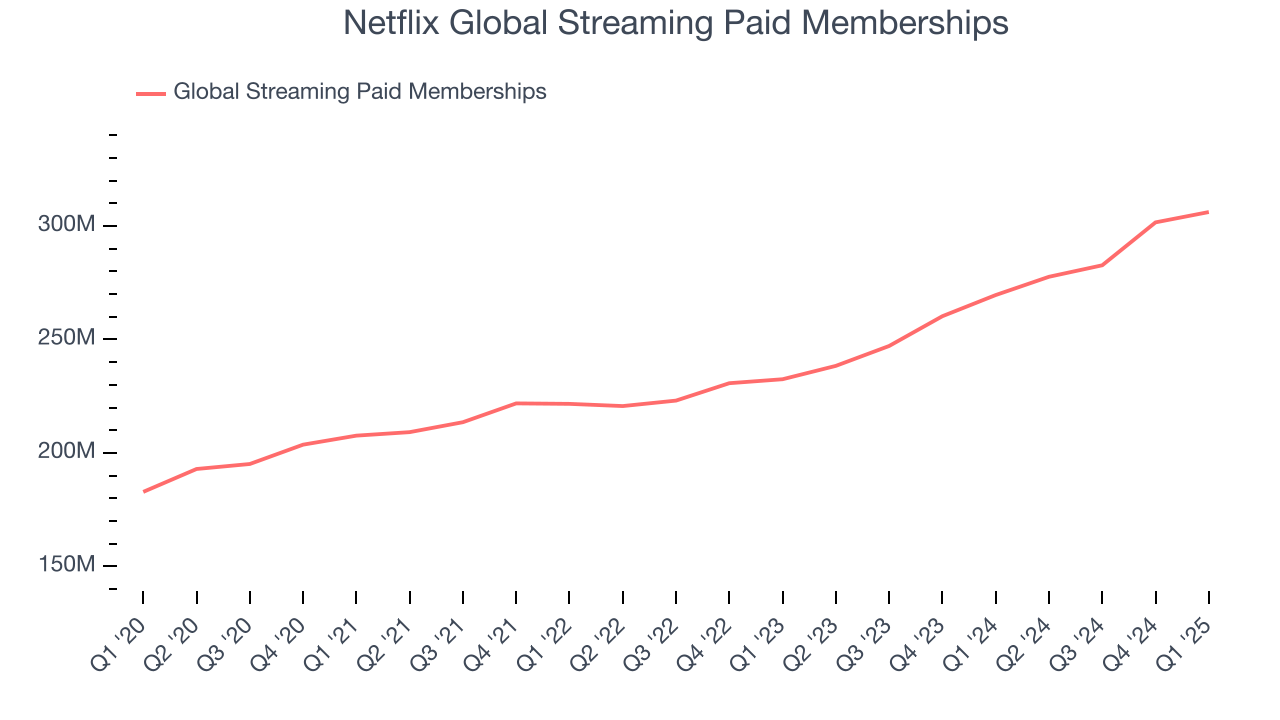

6. Global Streaming Paid Memberships

User Growth

As a subscription-based app, Netflix generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Netflix’s global streaming paid memberships, a key performance metric for the company, increased by 13.5% annually to 306.2 million in the latest quarter. This growth rate is strong for a consumer internet business and indicates people love using its offerings.

In Q1, Netflix added 36.58 million global streaming paid memberships, leading to 13.6% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the average user spends. ARPU is also a key indicator of how valuable its users are (and can be over time).

Netflix’s ARPU fell over the last two years, averaging 1.1% annual declines. This isn’t great, but the increase in global streaming paid memberships is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Netflix tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

This quarter, Netflix’s ARPU clocked in at $34.43. It was flat year on year, worse than the change in its global streaming paid memberships.

7. Gross Margin & Pricing Power

For internet subscription businesses like Netflix, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include customer service, data center and infrastructure expenses, royalties, and other content-related costs if the company’s offerings include features such as video or music.

Netflix’s gross margin is below the broader consumer internet industry, giving it less room to hire engineering talent that can develop new products and services. As you can see below, it averaged a 45.1% gross margin over the last two years. Said differently, Netflix had to pay a chunky $54.87 to its service providers for every $100 in revenue.

This quarter, Netflix’s gross profit margin was 50.1%, up 3.2 percentage points year on year. Netflix’s full-year margin has also been trending up over the past 12 months, increasing by 3.9 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

8. User Acquisition Efficiency

Consumer internet businesses like Netflix grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

Netflix is extremely efficient at acquiring new users, spending only 15.8% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a highly differentiated product offering and strong brand reputation from scale, giving Netflix the freedom to invest its resources into new growth initiatives while maintaining optionality.

9. EBITDA

Operating income is often evaluated to assess a company’s underlying profitability. In a similar vein, EBITDA is used to analyze consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a clearer view of the business’s profit potential.

Netflix has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 26%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Netflix’s EBITDA margin rose by 6.9 percentage points over the last few years, as its sales growth gave it operating leverage.

10. Earnings Per Share

We track the change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Netflix’s EPS grew at a spectacular 24.3% compounded annual growth rate over the last three years, higher than its 9.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Netflix’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Netflix’s EBITDA margin expanded by 6.9 percentage points over the last three years. On top of that, its share count shrank by 3.5%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q1, Netflix reported EPS at $6.61, up from $5.28 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Netflix’s full-year EPS of $21.16 to grow 23.2%.

11. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Netflix has shown robust cash profitability, driven by its cost-effective customer acquisition strategy that enables it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 19.2% over the last two years, quite impressive for a consumer internet business.

Taking a step back, we can see that Netflix’s margin expanded by 18.6 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Netflix’s free cash flow clocked in at $2.66 billion in Q1, equivalent to a 25.2% margin. This result was good as its margin was 2.4 percentage points higher than in the same quarter last year, building on its favorable historical trend.

12. Balance Sheet Assessment

Netflix reported $7.2 billion of cash and $15.02 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $11.72 billion of EBITDA over the last 12 months, we view Netflix’s 0.7× net-debt-to-EBITDA ratio as safe. We also see its $446.1 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Netflix’s Q1 Results

We were impressed by Netflix’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad this quarter's EPS exceeded Wall Street’s estimates. On the other hand, its full-year revenue guidance slightly missed, but next quarter's guidance was slightly above. Given the macro uncertainty with President Trump's tariffs, the market likely weighed the shorter-term guidance higher. Overall, this quarter had some key positives. The stock traded up 2.1% to $995.31 immediately following the results.

14. Is Now The Time To Buy Netflix?

Updated: June 16, 2025 at 10:21 PM EDT

When considering an investment in Netflix, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

There are several reasons why we think Netflix is a great business. Although its revenue growth was mediocre over the last three years, its growth over the next 12 months is expected to be higher. And while its ARPU has declined over the last two years, its impressive EBITDA margins show it has a highly efficient business model. In addition, Netflix’s rising cash profitability gives it more optionality.

Netflix’s EV/EBITDA ratio based on the next 12 months is 37.8x. Expectations are high given its premium multiple, but we’ll happily own Netflix as its fundamentals shine bright. It’s often wise to hold investments like this for at least three to five years, as the power of long-term compounding negates short-term price swings that can accompany high valuations.

Wall Street analysts have a consensus one-year price target of $1,158 on the company (compared to the current share price of $1,220).